The Trustee and The Gambler

Getting to know your split personality

If we’re honest, most us have a split personality when it comes to investing. Two distinctly different people. Each with their own motivations. Yet both are a real part of the person we think we know.

To be successful, or merely survive, you need to know them both intimately. If you don’t, they’ll overpower you. One of them can limit you. The other can destroy you.

I call these two personalities the trustee and the gambler. In my experience, the more I get to know and respect them, the greater my success. Once you see these in your life you may share my feeling.

Think of it like this. You’re driving and reach a fork in the road. You have a decision to make. To the left, smooth pavement, signs showing the distance to food, shelter, and your destination. To the right, pavement turns to gravel, then dirt, mud, and finally jungle. There’s no sign showing food, shelter, or the distance to anything. However, there’s a billboard advertising a chance at life-changing fortune somewhere ahead.

From where you sit now, this seems like a logical choice. Take the smooth road. Only a maniac would drive into what’s an obvious abyss. The risks far outweigh any treasure you might find.

Let’s raise the stakes. You’ve got your partner in the passenger seat, and a toddler in a car seat behind you. Imagine the kind of person who’d go on a reckless treasure hunt under those circumstances.

The Advantage of Knowing Your Split Personality

The point is, most people make money decisions they’d never consider in other parts of life.

They’ll avoid touching a bathroom door handle at all costs. They’ll buy overpriced insurance they’ll likely never use. They do many things that go against statistical odds. Only to become obsessed with a high-risk penny stock and gamble three years of savings hoping to make a fortune. Objectively, this makes no sense.

After the obvious and avoidable loss, they’ll look for someone to blame. Maybe it’s the source of the stock tip. Maybe it’s stocks all together, or the broker who enabled them to borrow on margin. Either way, blame is a great way to avoid looking at the facts. They either can’t look, or don’t want to know.

It took me a while to learn what was going on here. I’d try to help people see how their thinking made no sense. When I realized they didn’t want to see, regardless of what they say, everything started to make sense.

These days I’m eager to know what people think about things. I want to know who has more power at the moment, the trustee or the gambler. I want to know what they think is a great idea, and what’s a bad idea. I’m listening, watching, and keeping an eye on what’s hot in the eyes of the masses.

I’ll show you today how it’s usually an important indicator of what’s next. Once you see it the way I do you’ll begin noticing these indicators in your interactions with people.

A Quick Housekeeping Note

The response to the last issue was overwhelming. I’d like to thank everyone who helped me get The Tucker Letter up and running.

This is initially a free service. People tell me they need sources of truly independent market research now more than ever.

However, the feedback last week was so strong it’s clear we’ll need to transition to a subscription service sooner than expected.

As you’ll see today, I’ll begin showing you in the coming weeks what I’m doing personally, and in my role as a trustee, to navigate the current market.

It’s an unusual time. Interest rates are shooting higher, stocks look set to fall, and real estate seems stuck with an army of industry “experts” assuring onlookers it’ll be fine soon. This is a dangerous time for hard-earned money. The decisions you make in the coming months might have consequences years down the road.

Readers of The Tucker Letter will have a front row seat. They’ll see what I see, and what I do about it. Over time, I’ll show you how I take in what’s going on, what I look for, and how I make decisions. Sometimes I’m wrong, and you’ll see how I handle that too.

For people who’ve read my work before this is an obvious format. There’s no publisher, marketing team, or managing editor between my work and you. Every other Thursday you’ll get a note from me that’s about as direct as sitting down at my desk and having a real-time chat.

For those who’ve never heard of me, I realize subscribing might seem like a risk. I’d first suggest reading my book. That’s a lower-risk proposition, and a fun read. If that goes well, you’ll have until March 31, 2023 to take advantage of a one-time 50% off subscription offer.

You’ll notice I’m sending out these initial notes to get people up to speed. My hope is you’ll have a chance to see what I’m doing, and if it’s right for you.

However, I know it’s not for everyone. As discussed, we’re managing hard-earned wealth here. We’re not gambling. There will be times when taking higher levels of risk makes sense. That’s not today.

Thank you again for supporting this exciting launch. I hope you’ll join me so we can take this journey together.

Gambling With Bad Odds

As we get rolling, we’ll have two portfolios. The trustee portfolio will primarily hold stocks I’m buying for a trust where I am currently trustee. These are typically larger companies I like for a timely reason. I’ll explain that reason when introducing each. You’ll see what I see and my thinking behind the purchase.

Keep in mind, the role of trustee is to take care of funds on behalf of a beneficiary. That’s a great deal of responsibility. Sure, there will be losses occasionally, but risking a wipeout in hopes of a dramatic win is irresponsible.

The gambler will be our second portfolio. This is where riskier positions belong. Holdings we’d hope to see grow faster than the overall market have a place here. These carry greater risk. There are times when risk isn’t worth taking. Meaning, when every gambler thinks it’s a great bet, it likely isn’t. Their reckless enthusiasm sends the price to a level where even if it works out, the payout doesn’t match the risk.

I’ll show why I feel right now is one of the worst times to make risky bets I’ve ever seen. To be clear, even if the bets pay off, the upside barely tops the current return of a high-yield savings account.

Know When to Gamble and When to Sit Still

The trick is knowing when to bet. It’s usually when everyone you know believes it’s a bad time to bet.

We’re not going to run around doing the opposite of everyone for the sake of being different. The actual bet has to make sense.

Take real estate for instance. It’s hard to find a detractor today. Realtors, investors, contractors, all tell me the current trouble is just a blip. I ask if surging insurance, borrowing, regulatory, and other costs will adjust generationally low return expectations. They say no.

It’s generally not a good time to buy real estate. However, in 2009 I gambled my life savings on an at the time busted single family real estate market. I did the math. I had a formula. I felt if I sticked to it I’d earn ~20% on my all-cash investment as a landlord.

What you likely don’t know, and can’t imagine now, is nobody agreed with me.

What The Bottom Feels Like

In 2009, people reminded me real estate just crashed. They suggested I read the Wall Street Journal. They promised another crash was just ahead.

I stuck to my model. It was lonely. The cheapest house I bought was $10/sqft. I put another $10/sqft into repairs. With a total of ~$25,000 invested I rented it out for $800/month. Even then I wasn’t sure real estate would come back. I had to be happy with the cash return.

The truth is, I really do not like real estate. It’s a cave man business. By 2011 I’d had enough and went back to writing, researching, and doing what essentially got me here today.

But along the way, my real estate portfolio paid off.

Last year, I sold all of the houses. The overall gain including rent collected was about 1,000%, give or take.

I need to tell you that specific detail because last year was the exact opposite of what 2009 felt like. Remember, people ribbed me for trying to buy houses in 2009. I got similar comments for selling in 2022.

Notice the investing masses repelled real estate at the bottom, and suggested holding on at the top.

I expect it to grind sideways for a few years. Buyers used cheap debt to gobble up property. The recent surge in borrowing costs means prices might stagnate for years. It’s not a great time to take risk in real estate.

That said, let’s learn from my experience being criticized. When everyone thinks something is a great idea, watch out.

Why I Expect Stocks Fall 15-20% Before Summer

I hear people saying they expect a recession, stocks to fall, etc. Next breath, they ask me for a good stock tip.

Think about that… They expect bad business conditions. They expect the value of major companies to fall. They would like something to gamble on.

What this means is, they want action. They need action.

It’s hard to believe, but people truly want me to tell them something they can buy with the hopes of multiplying their meager savings. They’ll promise if it goes wrong, they won’t blame me. They say I’m so smart, surely I know something they can buy.

This tells me they have more money to lose. Collectively, there’s more money waiting to be lost gambling in the stock market.

I try to be delicate with these strangers. They’re destined to hurt themselves, and I don’t want to be part of that. They need a place to lose money, and someone to blame the inevitable loss on.

If I heard them say the market is rigged, bogus, a scam, I’d be encouraged. That would tell me this is a time to go big on risk. That’s not the case yet.

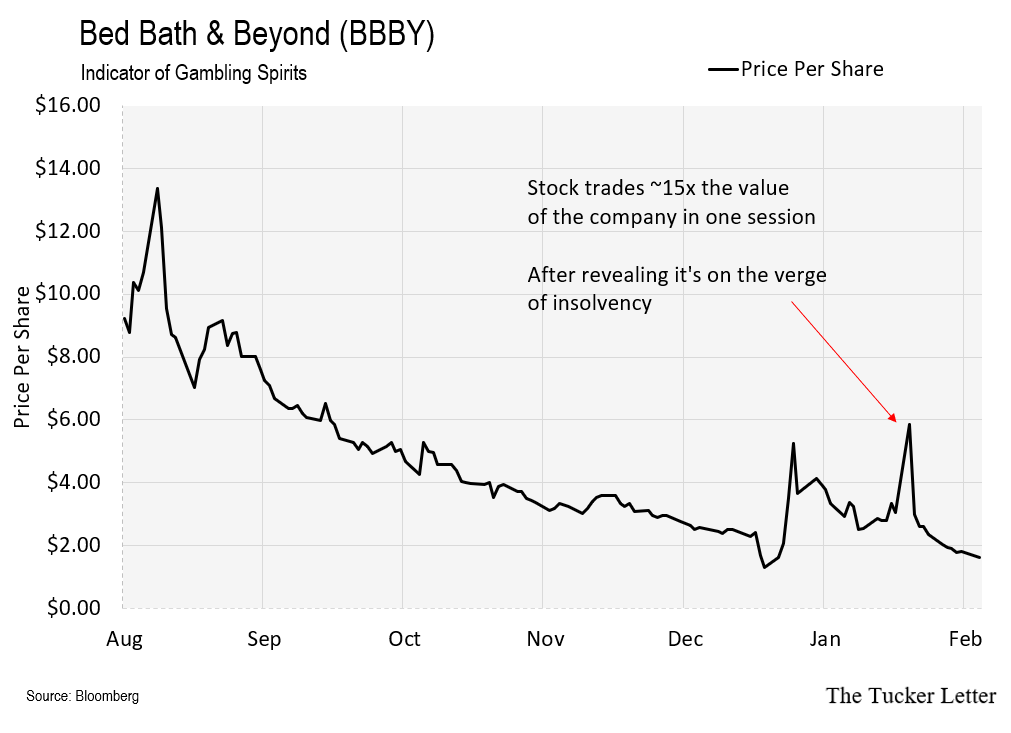

Take for instance, the recent surge in shares of Bed Bath & Beyond (BBBY). We’re not interested in the actual business of selling sheets and towels. Instead, the stock action tells us a lot about the state of the market right now.

Eager To Gamble with Terrible Odds

Bed Bath & Beyond (BBBY) is bankrupt. Well, maybe not completely bankrupt. It did manage to secure a desperate financing while in the process crushing its existing shareholders.

In order to see exactly how overzealous stock buyers are today, we need to look back at BBBY before it tumbled into trouble.

Couple of important memories about BBBY. When I wrote for a major financial newsletter ten years ago, we screened the market for companies with excessive free cash flow. That’s cash from operations less capital expenditures needed to keep the business up to date. It’s a measure of operational efficiency. BBBY was one of the highest free cash generators at the time.

Notice the period of 2009-2016 in the chart below. The company pumped out close to $1 billion in free cash flow annually. Again, that’s a measure of how much profit the company generated from operating the business, less necessary capital investment. For context, this level of efficiency is rare.

As you can see, the good times didn’t last.

The company used this excessive cash generating power to reduce its float. That’s finance jargon for buy back shares of its stock. It did this when the stock price hovered around all-time highs.

Again, we’re looking back to that magical period of 2013-16 when BBBY was a cash generating machine. We’ll get to the recent crash shortly.

BBBY had no debt when its stock hovered at all-time highs close to $80/share. The mechanics of this business were remarkable at the time.

However, I remember telling my colleague this was a terrible idea. He sparred with me over the subject. He was a Graham & Dodd type of “fundamental analyst.” These types get all the accolades, but rarely the capital gains. We’ll talk more in future issues about why this type of rigid thinking comforts people.

I admitted the BBBY story was virtuous, putting shareholders first, in appearance at least. But I reminded him of another retailer, Aeropostale, who spent its free cash flow buying back shares at a high price. During a recession it suddenly needed cash. It had to borrow. Debt service ate up shrinking profits. It went on to file bankruptcy.

Sure enough, BBBY ran aground doing the same thing. This chart shows debt per share from 2005 through last year. You’ll notice the company carried no debt through the years of heavy free cash flow.

In 2015 it takes on some debt, progressively more, then substantially more during the pandemic and recovery.

With no member of management reporting a tenure much longer than 2 years currently, BBBY hopes to stay afloat. It recently financed that hope at the Wall Street version of a pawn shop. While crushing for existing shareholders, management bought itself the opportunity to turn things around.

More Pain to Come

We don’t care much about BBBY. If you have a drawer full of their iconic 20% off direct mail coupons, use them quickly.

In our case, the recent action in BBBY tells us average investors have more money to lose in the market. Remember, it’s not a bottom until people swear off stocks for good. We’ll hear them blame people for their losses. They’ll invoke extreme personal austerity as a misguided form of penance. I don’t see any of that happening yet.

As evidence, notice the more recent chart below of BBBY going back six months.

Keep in mind, the company announced news it was teetering on the brink of insolvency. Its 2024 bonds traded down to $0.05 on the dollar having been fully valued just last March.

That’s a 95% collapse in the value its debt. Debt has greater security than stock if the company fails. Even with that extra security, debt holders wanted nothing to do with BBBY. Gamblers looking for action in the stock market did.

After all this recent news, retail stock investors rushed to buy BBBY shares hand over fist. They either don’t know, or don’t care what happens to stockholders if the company goes bankrupt. They get nothing.

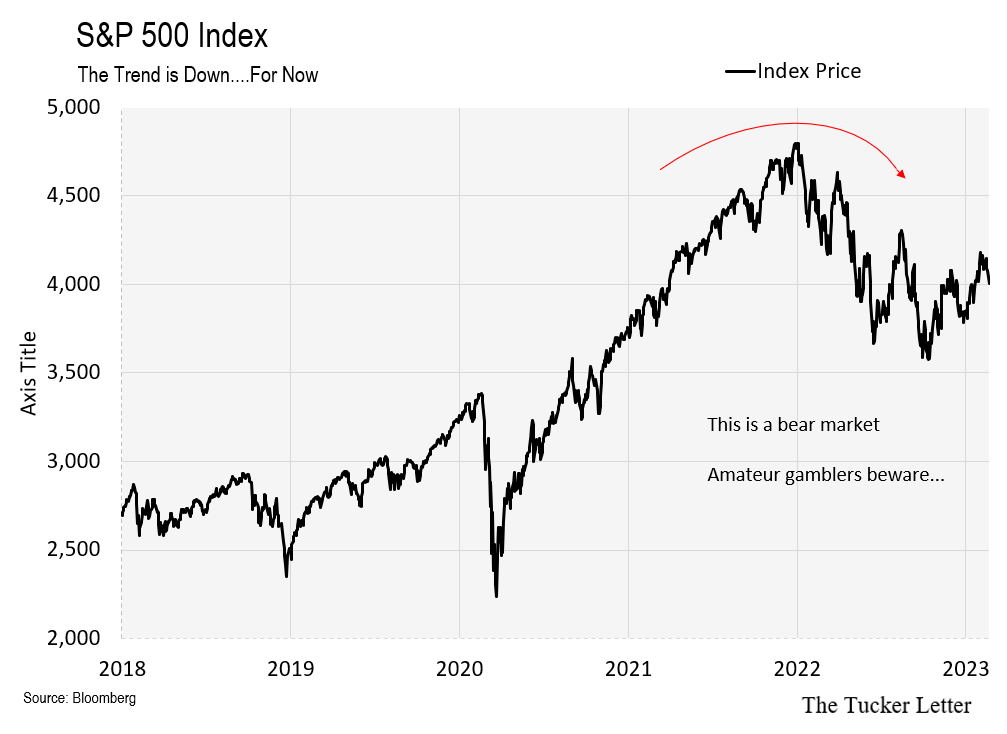

You can bet the average recent buyer of BBBY shares fits the profile of the strangers who ask me for a gambling tip. FOMO, YOLO, and other memes are the war cry of this disaffected group of gamblers. They either made money or had fun playing with stocks during the pandemic lockdowns. That was one of the most epic stock market tops of our lifetime. Today, we’re in a bear market.

Bear Markets Are a Bad Time to Gamble

As mentioned, we’ll have two portfolios in The Tucker Letter. One is the trustee portfolio. It holds stocks I’d own in the role of trustee.

If you’re a self-admitted gambler, this might sound boring. Trust me, it’s anything but. One stock I bought in November as trustee just hit an all-time high after climbing 20% in three months. I’ll show you why I bought it and am happy to hold it during a volatile period in the economy in another post.

The other portfolio will be the gambler. Over time, that portfolio would hold riskier bets. These are companies with big upside potential but sensitivity to market cycles and overall economic conditions.

During a speculative period, these companies do quite well. During a downturn, they face extreme risk. They often lack the structure needed to remain independent through tough times. This is not a great time to speculate generally.

In the meantime, take note of the sentiment you encounter when talking to friends and strangers. See if their actions match their words. See if their enthusiasm for gambling matches the tumble underway in the chart below.

At the real bottom, they’ll swear off stocks for good. Until then, be a trustee. Not a gambler.

Back with more in two weeks.

Every two weeks seems like a low cadence. What made you decide to publish twice a month rather than more frequently or less often?

Just joined and will be a regular. Looking forward to your letters.