The Frankenstein Economy

When too much control backfires

Bryan Johnson sleeps alone with a monitor strapped to his penis.

In a quest to live forever, the 46-year-old aims not only to stop the aging process, he wants to reverse it. If successful, he’ll outlive his unborn grandchildren.

Johnson’s health “Blueprint” controls even the most mundane parts of life. It’s an almost unimaginable level of asceticism. He calls inadequate sleep, snacks, and minor everyday poor choices “acts of violence.”

Showing a remarkable level of self-awareness, he admits he is impossible to date. Even with a 9-figure net worth, he realizes no human can live with someone who:

· Collects his own stool samples

· Takes 111 supplement pills daily

· Wears a special red light-emitting baseball cap

· Eats dinner at 11:30 AM

· Avoids the sun

· Goes to bed at 8:30 PM

· Ignores small talk

· Sleeps alone (with the monitor attached)

· Prioritizes his quest for eternal life over human relations

It’s normal to hope you outlive the average. Nobody wants to be the first to drop. But living forever doesn’t make much sense. Especially if you avoid human interactions to do it. Celebrating your 300th birthday alone with the curtains drawn doesn’t sound like fun.

Weird Outcomes

Nothing is permanent. It’s a tough concept, but it’s irrefutable.

Everything has a lifecycle, it’s what makes things interesting. From rocks and trees to corporations and people, there’s a natural process at work.

Birth is exciting. Green shoots, the big bang, joyful parents, in each case it’s an explosion of new energy. Then comes growth, maturity, and feeling firmly rooted, for a while at least. Then death, which makes room for the exciting process to start over.

The problem is, we don’t like change. It makes us uncomfortable. For some reason it causes a lot of stress.

During that mature period, we try to make things permanent. It never works. Plastic orchids in bloom year-round don’t produce the same feeling as a brief glimpse of the real thing. There’s a magic in watching life unfold naturally.

Trying to stop the process, freeze it permanently, or reverse it, creates weird outcomes. In the case of Bryan Johnson, the quest for health seems unhealthy.

Born in 1977, his driver’s license says he’s 46. However, constant monitoring and testing support his claim that some of his organs are now much younger.

Time will tell if this protocol leads to a better life. It seems extreme.

The thing about living at the extremes is it’s not what you fear that gets you. It’s something random you didn’t see coming.

An Ounce of Prevention

Johnson admits there’d be great irony if he were t-boned while driving in Los Angeles. This shows he does have some sense of reality.

I sympathize with his health quest, generally. While I don’t sleep with any monitors attached, people close to me do describe me as a health nut. I enjoy learning about health, adjusting my lifestyle, habits, and food choices, all for a better life.

However, the goal of my health journey is to live comfortably until I don’t live anymore. That means getting around without discomfort, feeling well, and being able to participate in life as it unfolds.

While I may eat at odd times, avoid foods most people love, and spend a fortune on the purest spring water in America, I’m not going for perfection. I want to live a balanced life. To prevent living at an extreme, I have the occasional treat.

Last week I stopped at La Cabra, a Danish bakery on 2nd Avenue in New York City’s lower east side for just this reason. I think they have the best chocolate croissant in New York. I’ve done extensive research in coming to this conclusion.

Chocolate croissant, or pain au chocolat, is difficult to make. La Cabra nails it. Notice how perfect it looks. There must be 100 layers of delicate flakes in their pastry dough, all cooked evenly. Including the tiny chocolate batons in the middle, the whole thing can’t weigh more than a postcard.

I don’t compromise when it comes to treats. I never eat anything from a package. If I can’t find something suitable, I’ll skip altogether and enjoy an extended fast. It’s either the best, or nothing.

Bryan Johnson considers my recent treat an act of violence. Maybe so. I can’t argue it’s a good decision. But I enjoyed it, and it reminded me I’m alive.

The Frankenstein Economy

Trying to control and manage the economy also leads to weird outcomes.

An economic system is a living, breathing marketplace. Buyers and sellers, savers and borrowers, negotiate with each other every time they consummate a transaction.

Millions of transactions happening every day mean people effectively choose to conduct business at the best price. We call the result the “market price.” It’s something that only exists in a free market system.

For decades we told the world our system was the best, the most fair. It made us superior to the Soviets. Those cold operators behind the iron curtain controlled their economy by central committee. The result, inferior products, unhappy people, and a less enjoyable life.

One downside of the free market system is recessions. Like forest fires, they clear out dead debris, clutter, making room for the strong to thrive. Green shoots, healthier trees, and a stronger forest emerge after the fire. Efficient, well-capitalized businesses emerged after each recession.

We all remember the recessions of last century. Business slowed, everyone felt it. Companies with too much debt or poor business models failed.

We had one of these recessions every decade or so. While it meant pain for overextended or sloppy operators, it seemed normal. The lesson was, be careful taking too much risk. It seemed to keep greed in check.

Those days are over. In the late 1990s the Fed started managing the business cycle. It figured capitalism in its pure form had too many variables. A little management would smooth things out, reduce the pain.

Politicians Don’t Like Recessions

Free markets are harsh. Recessions lead to layoffs, foreclosures, and hard times for the most overextended.

The fed and its political allies naturally don’t like things they can’t control. You can imagine the incentive to create a perpetual, controlled boom. An economy with only upside, no downside. That’s the goal at least.

This is the economic equivalent of people who fear being sad. Notice when people ask you how it’s going, the only acceptable answer is, “Great!” If you say you’re sad, they seem deeply uncomfortable.

But sad and happy are two sides of the same coin. You can’t have a coin with heads on both sides. It loses its meaning. And you can’t have perpetual growth with no natural restraint.

All the talk and national pride behind the free market system seems misguided.

For instance, you’d assume the people with savings decide how much to charge borrowers. After all, saving that money took a lot of hard work, sacrifice, and discipline. In a free market, savers decide if the interest rate on offer matches the value of their capital.

These days, we wait for a committee to tell us how much we earn on savings. The committee decides in secret. It occasionally bails out profligate borrowers. Nobody knows why some get a bailout, and others fail.

From the outside, this doesn’t look like capitalism. It’s a state-controlled market. We no longer have recessions. We have a perpetual boom with the occasional panic.

During the 2020 virus panic the U.S. stock market lost ~35% of its value in about three weeks. At the time, that meant about ~$13 trillion of value vanished.

The central planning committee stepped in buying a varied assortment of debt instruments. It stabilized some parts of the market. Prices of the purest junk imaginable pivoted on a dime. Anyone betting on failure got their head chopped off. Not by the market, by a committee.

The question last century was when will we have a recession. All the tools used to answer that question are useless.

In the Frankenstein economy it’s all about predicting what the committee does next.

Old Tools Can’t Help Us Predict What’s Next

Take a look at this equation. It’s the latest Fed tool used to decide if inflation is a problem for you.

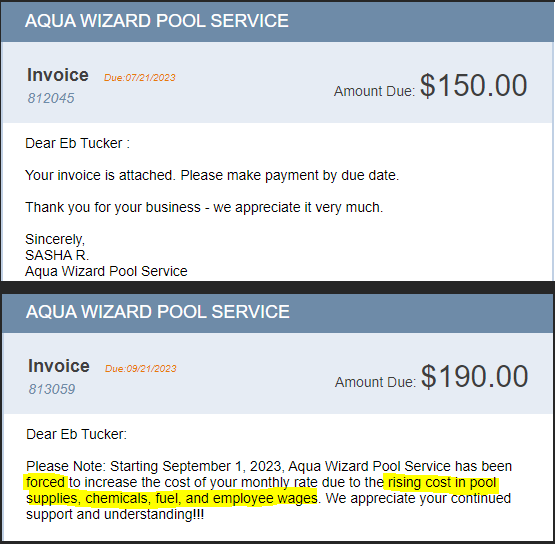

I’ve got a better indicator….the aqua wizard.

We already know Mark, the aqua wizard, is a guru. Wise beyond even his own understanding, he pretends to be a humble pool servant. As we discussed this summer, he knows what the fed is up to.

The wizard sent me this note recently. He doesn’t use fancy math equations to calculate rising prices. He simply tallies the rising cost of doing business and passes it on to customers.

That’s a ~27% increase in real costs. Meanwhile, the fed continues to use its complex shell game to disguise inflation. It now measures something called “Super Core” inflation. This gives it a new metric to show you everything is fine.

The trick here is keep removing variables until the inflation rate looks flat. Year to year that is. Over the long term, inflation is a one-way street.

And it has to be. The fed needs inflation. As long as you don’t catch on, it keeps ratcheting up prices.

Don’t mistake this for thrifty behavior. There’s no intention of balancing a budget, reducing debt over the long term, or being fiscally responsible the way you and I know it. Instead, inflation helps the fed reduce the cost of paying down debt….so it can issue more debt.

The fed’s reason for debt reduction is to load the cannon for the next stimulus. It can’t juice the economy without making some room. Notice how its debt pile shrinks a bit, then explodes at each crisis.

While the shrinking periods look small on the chart, remember they once appeared large. The fed’s debt pile grew from ~$800 billion to ~$9 trillion over the first two decades of this century.

And it’s about to grow again. But we can’t use old tools to predict when.

New Tools for State-Controlled Capitalism

The U.S. government is a hungry borrower. According to the Wall Street Journal, the Treasury Department borrowed a net $1.76 trillion during the first 9 months of 2023.

We all know the facts. Congressional officials spend every cent they extract from us plus another ~$2.5 trillion they borrow from the future. That’s tax they plan to extract from our progeny.

If we had a true free market, where lenders decided if it’s a good risk to take, this might be a problem. But we don’t. The fed steps in to support its enabler, the Treasury. Until now at least.

The record issuance of treasury debt is a python eating a pig. With short term interest rates elevated, the lending market looks broken.

For instance, if tie your money up for 12-months you’d assume a lower interest rate than the same loan for 120-months.

The logic here is, the longer someone has your money, the more interest you expect to receive.

After all, a 30-year fixed rate mortgage usually costs more than a 5-year fixed rate mortgage.

This is sensible, in a free market. But the U.S. Treasury now pays substantially more to borrow for 6-months than it does for 5-years. This is the sign of a broken market.

Here’s what a hypothetical borrowing schedule should look like. Forget about the exact percentages for a minute, it should cost more to borrow for longer periods of time.

While we can’t know for certain, the fed likely wants to sort this out. Not because they want to help you… it’s a matter of maintaining control.

And it better do it quickly, before the American homeowner loses patience.

You may notice people don’t want to move. I hear this all the time. People say they’ll never let go of the ~3% mortgage they took out a few years back. Who can blame them…

But the American home is ~20% of the economy now. If nobody moves, that 20% stops contributing to growth. No realtor commissions, title company fees, or municipal taxes on property transfers. It’s a big deal.

This puts the fed and the Congress in a bind. Tax receipts don’t look good this year. Congress aims to spend ~$2.5 trillion more than it collects.

While the fed tries to keep its price fixing scheme intact, we see the pressure building in odd places.

Bridge Out Ahead

What feels like calm today faces a major reality check before spring of 2024.

The numbers simply don’t work. Old indicators won’t help us. We need a new way of thinking to see what’s barreling down the pike.

Subscribers know we have five important themes working in the Trustee Portfolio directly related to what’s ahead.

It’s not a time to gamble. The days of SPACS, junk penny stocks, PancakeCoin, and excessive risk taking are over. They will be back, but it’s the trustee who wins in this environment.

That means the right portfolio:

1. Directly benefits from surging borrowing costs. We have little to no concern about the treasury repayment risk over a 4-week or 8-week time horizon.

2. Pays attention to the ~90% of world energy supplies not controlled by the U.S. We have three stocks tied to oil and none are production companies.

3. Owns products people can’t live without. Supersized Americans don’t realize food is a drug. Salted fried food being the most addictive. Those that do choose better ingredients favor smart shopping. We own both.

4. Owns the American war machine, which flared up last weekend sending one stock up ~8% Monday. The tools of war change almost quarterly now. This is a race to stay safe, we want to own that...even if we disagree with fighting in principle.

5. Owns big picture industrials that benefit from rising costs.

Nowhere in there is it sensible to own speculative, overnight sensations. That’s what you do in a time like 2021. Listen to the aqua wizard…. When they drain the pool, it’s not a good time to swim.