Drain The Pool

Wise words from The Aqua Wizard

The Aqua Wizard hovered in front of my office window until he had my full attention.

“Mr. Tucker, we gotta drain the pool for a bit. Rained a bunch while you were gone.”

My office faces the end of the pool. Mark is the best pool guy I’ve had. When I replaced the prior service, he introduced himself as “The Aqua Wizard.”

The wizard went on to explain in great detail why we had to drain the pool. He showed me the five rectangular tiles at the top of the pool. He called them waterline tiles. He wants the water level on the middle tile of the five tiles….and for good reason.

If the water level is too high, the pool overflows. It’s like overfilling a cup. It might loosen the limestone pavers or cause other issues around the pool. The excess water has to go somewhere. It’s a mess. During the rainy season he wants to avoid this by draining the excess water.

But not too much. If the water level drops below the waterline tiles, the pool could crack. The wizard explains physics.

“The pool shell relies on the pressure of the water…if it drops too low the shell cracks, we don’t want that.”

We absolutely don’t want that. It means structural problems. A cracked pool isn’t a pool anymore, it’s a nuisance.

Managing Physics

All we have to do is manage nature. It’s not too hard.

It rains almost daily in the summer here. Like clockwork, every afternoon we get hit. That keeps the pool full from June to October.

In the winter, it’s dry. The wizard runs the hose to keep the level up. He outsmarts nature. And he does it all while listening to his headphones. From my view, he has the best job in the world.

I wonder if the wizard would manage so gracefully if people were involved. If filling the pool made people want to throw a pool party. And draining the pool did the opposite, made people disgruntled, caused them to leave the party. He probably wouldn’t make it look so easy.

Managing nature is harder with people involved. It changes the incentives. They respond by changing their behavior. They get used to the new way of doing things. When that changes, they don’t like it.

People Don’t Like Discomfort

A long time ago we had occasional periods of discomfort. We called them recessions. Essentially, business slowed. Profligate spenders, irresponsible types, ran into trouble. Some went bankrupt. Overextended businesses closed. When the dust cleared, things got better. There was a reward for being responsible with money decisions.

Recessions are part of capitalism. It’s a natural way of purging inefficiencies. People decide to take risks. They calculate how much they can handle. The threat of recession helped keep them focused. It kept them serious about what could go wrong.

Those days are over. We no longer have recessions. Instead, we have a sustained boom with the occasional, brief, panic.

It’s almost as if the U.S. central planners decided free markets were more trouble than their worth. From the recessions to the shifting price of assets, the whole thing made it hard to control people.

“Capitalism Lite”

Most people believe the U.S. is a free market economic system. They’ll tell you all about it if asked. But they’re wrong.

What we have is an economic system run by committee. It’s centrally controlled. You could call it “capitalism lite.” It looks like capitalism to the casual observer. But it’s far from the real thing.

In a free market, prices set themselves. Buyers decide where they’ll shop, what they’ll pay, and who they’ll deal with. The best product, service, or experience wins the most customers. Over time, that business reaps benefits. Eventually competition takes hold. The system runs itself.

Instead of that, we now have giant swaths of the U.S. economy operating under committee control. Take housing for instance. It’s ~20% of the economy now. Realtors, insurance agents, title companies, contractors, all see themselves as capitalists. However, the real estate business lives and dies by interest rates, set by committee. If it were a free market, independent lenders would decide the interest rate paid by borrowers.

Or take medical care. That’s another ~20% of the economy controlled by bureaucrats. Nobody understands the actual cost of medical services. From HIPAA forms to the love affair with ineffective medical insurance, the U.S. medical system would crumble in a truly capitalist free market.

Instead of letting the free market work out inefficiencies, central planners wanted a slow drip type of capitalism. By controlling the flow of credit into the economy, they want a permanent slow-motion boom.

The benefits of this are great for people in power. The lower classes barely feel it. Even better, they see the value of their assets rise consistently. It’s a great distraction. Economists call it, “The wealth effect.”

A Great Plan…. So Far

The plan went like this. The Fed would dictate borrowing costs replacing the frugal savers of last century. In order to keep the system growing, borrowing costs needed to slowly fall. Real estate and private equity investors stood to gain the most. Stock and bond investors should win too.

Take a 100-unit apartment complex for instance. Say it costs $1 million back in 2000. An investor puts $200,000 down and borrows $800,000 at ~7%. The closing agent, bank, and local construction crews all benefit.

A year goes by. The Fed fixes interest rates down a point to ~6%. Apartment rent hasn’t budged. Not much changed other than interest rates. A new buyer runs the numbers. He can pay ~$1.1 million for the same 100-unit complex and pay the same amount of interest.

The owner sells to a new buyer booking a $100,000 gain. The closing agent, new bank, and the next owner’s construction crews all benefit. Each time interest rates fall this property changes hands in a profitable transaction. Everyone connected to the property in some way gets paid, pays taxes, and thinks the real estate business is great.

The problem with this is, nothing actually happened. The owner didn’t create anything. He merely paid bank interest for a while before selling to the next owner at a higher price. The apartments didn’t change much outside of paint, a new fridge, or the occasional new roof.

The same thing went on in the stock market. Consistently falling interest rates made borrowing easier. Companies producing tangible goods didn’t change much. The cheaper money made speculative ideas easier to fund. This chart tracks the total value of all U.S. publicly traded stocks through 2020.

These were the good years of the Fed’s command and control policy. It seemed like nothing could go wrong. The problem was, they still had human nature to deal with. Lurking at every market panic were smart, opportunistic borrowers ready to take advantage of their connection to the central planning committee.

People Expect the Rescue Crew

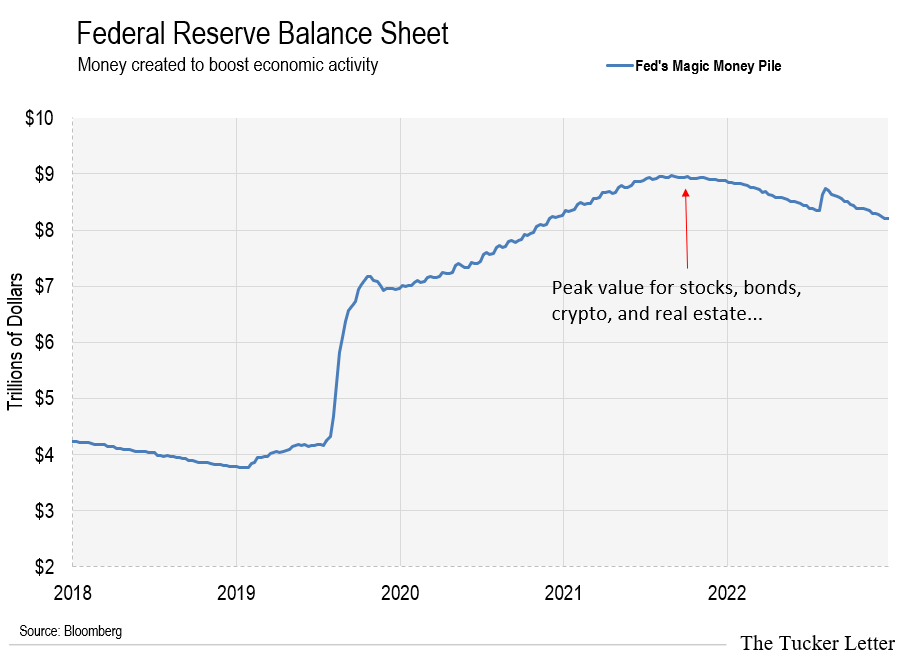

By 2020 the numbers seemed huge. The Fed’s balance sheet swelled from ~$800 billion in the late 1990s to over ~$9 trillion.

The real issue isn’t the size. This number will grow and grow. A future generation may look at $9 trillion as a drop in the bucket. The only limit to the Fed’s experiment is people’s willingness to go along with it.

Fed action in 2020 reached dangerous levels. It bought distressed loans, mailed three rounds of checks to low-income earners, and loaned money to anyone with a tax ID in the name of “payroll protection.”

This record pile of free cash found its way into odd corners of the market. In late 2021 these markets all hit unusual highs almost simultaneously:

· Bitcoin

· Junk Crypto Coins

· SPACs

· Meme Stocks

· FANG Stocks

· Real Estate

· Treasury Bonds

None of the prices made sense. Almost two years later, most of them are far off all-time highs.

· Bitcoin (XBT) -57%

· Junk Crypto Coin Index (XAI) -77%

· SPAC Index (SPAC) -24%

· Meme Stock Index (MEME) -57%

· FANG Stock Index (NYFANG) -5%

· Real Estate ETF (VNQ) -30%

· Treasury Bond 20yr ETF (TLT) -39%

While most investors still want a tip on the next stock, crypto, or real estate deal, this is a bear market.

With the performance of speculative assets hitting new lows, investors somehow think they’ll outsmart the bear market. It doesn’t work that way.

The reason is, the market goes where the central planners tell it to. This chart shows the Fed’s money pile hit a peak almost the same time speculative asset values peaked.

In addition to raising interest rates from 0% to 5.5% in record time, the Fed also stopped buying treasury and mortgage bonds. This change meant no new cash flooding into those markets. Treasury borrowing costs began to rise. Mortgage borrowing costs followed suit.

The stock market also needs cheap money to charge higher. Notice in the chart below, stock values peaked when the Fed’s money pile peaked.

There was a partial recovery in 2023 but now values look set to fall again.

The Fed Created Dependency

It’s too late. Once you engage in market gamesmanship, there’s no turning back. The economy, bonds, stocks, real estate, crypto, or any other market can’t detach from the Fed’s radical money experiment.

The Fed’s current plan is to drain the pool until they see a crack. When they do, they’ll come up with another rescue program. It won’t look like the last one. It’ll benefit the most connected players in high finance.

Barry Sternlicht of Starwood Capital Group thinks he has this figured out. On July 18th he defaulted on a bad investment tied to an Atlanta office tower. Just a few days later he went on Bloomberg TV with private equity baron David Rubenstein to share his excitement about buying distressed real estate in advance of the next radical Fed action.

The Fed created this behavior. Sternlicht can borrow without consequences to buy speculative assets. He has no interest in owning them if the market declines. He’ll stop paying the mortgage and walk away. Heads he wins, tails he walks away.

If You Don’t Have That Luxury

Our job between now and then is to stay out of the crossfire.