More Dangerous Than the Minneapolis Light Rail

Investing for the past

The young woman jumped onto the train as if she was being chased. She was.

Running close behind on the 50th Street platform was what appeared to be her pimp. As he slipped through the closing doors, she looked panicked.

The train is more dangerous than the platform. There’s nowhere to run. The pimp approached, snatched her backpack, emptied it on the floor. Then, inches from her face shouted, “Where’s the rest of it?”

When the doors opened at 46th Street the girl hopped out and into the next car. That’s the last I saw of them.

It’s just another weekday afternoon on the blue line. One of two trains making up the Minneapolis light rail system. Google Maps suggested I take it from MSP airport to my downtown hotel last week.

I like public transit. It’s typically better than sitting in traffic with a talkative Uber driver whose car smells like a cheap air freshener.

That’s not the case in Minneapolis. The multi-billion-dollar light rail system is an airconditioned crime scene.

I had seven stops left when the angry pimp switched cars. He left the girl’s backpack and its contents on the train floor.

Three men in their 50s boarded at 38th Street. One pulled a pint of Seagram’s vodka from his pocket. The second had a brown bag with a 750ml glass bottle of Smirnoff. They ridiculed the third as he produced a plastic bottle of New Amsterdam, evidently a down-market brand. Vodka seems to be the drink of choice on the blue line.

With U.S. Bank stadium in view, we had 3 stops left. I might live. A scrawny young man in dirt-stained clothes boards with a gorgeous Cannondale road bike. Easily $4,000 retail. The vodka crew offers $20. He wants more, at least $50. The platform at the stadium station looks like a war zone. Nobody seems concerned.

What Google Maps didn’t tell me is the Twin Cities light rail system is the most dangerous in America.

Things got tense as we approached the first downtown station, Government Plaza. Groups shouted across the car about what they’d do to a white person if given the chance. I opted to disembark and walk the rest of the way.

Feeling like I just left horror movie, I recounted the incident to the hotel clerk. She said, “Yeah, nobody rides that thing.”

Cheap Debt Made It All Possible

Blood-stained, chronically over budget, and fully outfitted for disabled passengers, the Minneapolis light rail runs through a downtown built for yesterday.

Minnesota has one asset of strategic importance, the Mississippi river. It runs through the heart of Minneapolis. Without it, the place might not exist. Maybe we don’t need rivers anymore. Or nature in any form. Time will tell…

Minnesotans pay a hefty price for residency. Personal income tax rates top out at 9.85%. Sales tax runs as high as 8.875%. There’s a corporate tax of 9.8%. The state ranks 45th in the nation when it comes to tax according to the Tax Foundation. The light rail passengers don’t seem concerned.

I had business in the Midwest last week, South Dakota specifically. It’s hard to get in and out of there on commercial airlines. I stopped in Minneapolis on the way back to break up the trip.

Once out of the downtown hellscape, Minneapolis does have redeeming features. The September weather is perfect. There can’t be more than 1,000 feet between lakes in the residential neighborhoods. Lined with charming homes, it looks like an ideal lifestyle. At least until winter sets in.

For instance, there’s a tony suburb southwest of downtown called Fulton. You won’t see it on the list of light rail stops. That’s where I went Wednesday night. In fact, it’s the main reason I wanted to stop in Minneapolis.

The Importance of “Sitting” Still

Fulton is home to a Zen center called Dharma Field. It’s on the corner of a quiet residential street, you’d drive right by if you weren’t looking for it. I’d visited once before, several years ago, for a Wednesday night sitting.

You might not be familiar with what goes on at a Zen center, much less a sitting. Here’s how it works.

The session begins promptly at 7:00 PM. If you’re late, nobody cares, just take off your shoes and enter quietly.

There’s a large room with no furniture. At most, you’ll see a small shrine. Dharma Field has shrine made up of a large rock, a few flowers, and a candle.

Around the perimeter of the room are cushions, about 2-feet square. There’s a round cushion on top of those. You walk in quietly, sit on the cushion, and face the wall.

The monk taps an antique brass bowl three times. This starts the meditation. With eyes open, you stare at the wall for thirty minutes. That’s right, thirty minutes.

Most Americans can’t imagine sitting still without a smartphone for this long. That might partially explain the current societal obsession with being anxious.

Even the model pictured on the magazine cover seems anxious. Her hands positioned to calm a racing pulse, or stop a gasping for breath. She appears to be thinking about working out, or taking a golden retriever hostage, or lavender. Whatever she’s trying to do, sitting still would likely fix her problem.

Sitting works. For me at least.

There’s nothing to do when sitting. Thoughts rush into your head. If you don’t do anything, they rush out just as fast. One breath after another this goes on until you can’t remember what you were worried about moments ago.

After a half hour, the monk hits the bowl again like a chime. Session over. Everyone exits the room quietly in a single-file line.

After the sitting, Dharma Field offers a one-hour topic discussion. Last week it was a chapter about flowers in Dhammapada. It’s a well-known ancient book.

Before my kids wake up on weekend mornings, I’ll escape to my office with a coffee and read a page or two of this book. It’s nothing cosmic, but it forces me to slow down and think about something other than the urgent tasks ahead.

Transition Periods are Dangerous for Investors

After the discussion I had a quick chat with Roger. He’s in his 80s. He doesn’t miss any of these weekly discussions.

Roger told me, “It’s our beliefs that cause most of our trouble.”

Bingo…

I don’t know if Roger is a stock investor. But he just nailed a big problem.

We believe in the last bull market. We watched it happen; we understand it like last weekend’s football game. But it’s over. And that means the trades that worked well during that period are over too.

Waiting Out the Transition

These are just a few of the features of the bull market we just lived through:

· 0% interest rates

· Easy credit terms

· Lots of credit!

· Cheap mortgages

· Lots of capital for high-risk startups

· Lots of IPOs, SPACs, and hot stocks

· Cheap energy

· Digital tokens with pictures of apes on boats

· 0% money means a projected return >0% finds an investor

Think about each of these factors individually. Not one of them is happening right now.

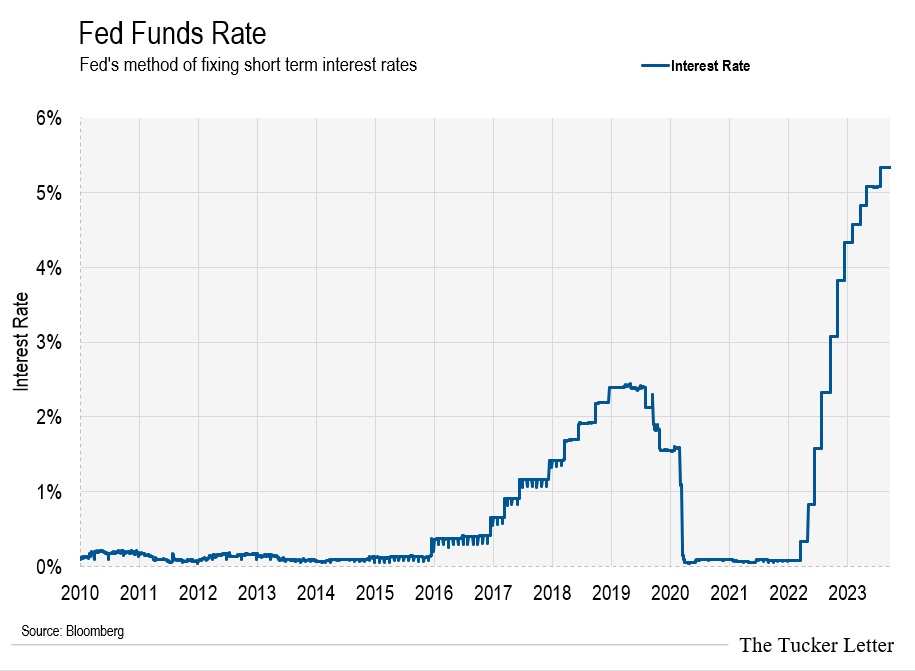

For starters, interest rates shot from 0% to 5.3% almost overnight.

Credit terms changed for borrowers. Ask homeowners, car buyers, shoppers, or businesses trying to borrow. You can find the money, but you’ll pay for it.

While the Fed fixes short-term interest rates, lenders decide how much money costs over the longer term. That rate is up.

With the 10-year treasury as a baseline, it looks set to go even higher. This could easily hit ~6% in the coming quarters.

Surging 10-year treasury rates were unthinkable during the last bull market. Notice 2020 in the chart above. The rate hugged ~0.50% for much of the year.

Many people took out home loans for ~3%. Today the mortgage rate is more like ~8%....and rising.

People say real estate always goes up. It’s true, if credit keeps flowing. That was the case during the last bull market.

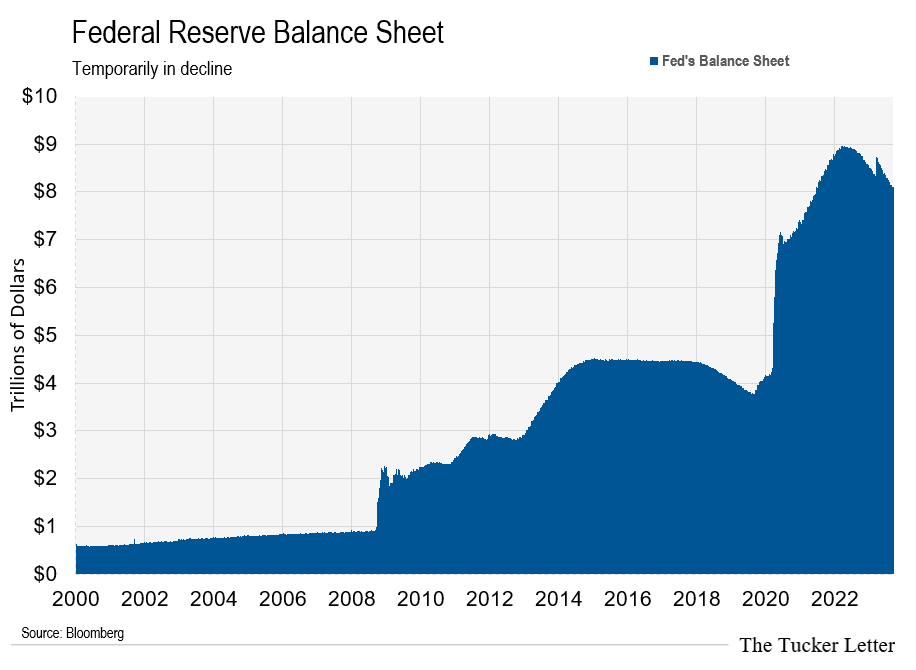

In fact, it was the case for more than twenty years. The Fed got us used to ultra-cheap money at the turn of the century. Every hiccup in the economy saw the Fed chair rush to the money spigot.

Like lab rats, we saw what the guy in the white coat did when we panicked. After a while, we forgot why we panicked. Every idea works when fresh new money comes in to fix bad investments.

Notice how the Fed’s balance sheet grew consistently for twenty years. Then, flipped on a dime to shrink as it cranked rates from 0% to ~5.3% almost overnight.

The problem is, people don’t realize the spigot is in the off position.

The Wheel of Debt

The math is simple.

Say you borrow $100,000 at 1% for five years. That’s $1,000/yr of interest expense. Year five rolls around. You don’t have $100,000 for the payoff so you need a replacement loan. Rates are now 10%. The new interest expense, $10,000/yr.

If your business grew during the five year loan period, you can probably handle the higher interest expense. If you spent the money on projects that didn’t pan out, you’re in trouble.

Now think about this on a global scale. Since 2000, the total amount of debt piled on the world economy grew at ~6%. That means every year, there was more debt available to finance the next idea, expansion, or to just keep people swiping their credit cards.

Projects like the chronically overbudget Minneapolis light rail found willing lenders every time it ran out of cash. Which was often.

Even the craziest ideas worked with 0% money. But the money stopped, and people can’t figure out what happens next.

If the debt pile growing at 6% each year made the economy grow, turning it off makes it stop. It’s musical chairs. No new debt and higher interest costs mean less chairs to sit in when the music stops.

Minneapolis needs billions more to expand its bankrupt light rail. They don’t even have ticket enforcement. When it comes back to the well to borrow, the numbers won’t work.

High borrowing costs mean projects have to work to get funding. Imagine what the people using the light rail as a homeless shelter will do when forced to buy a $2.50 ticket.

The Trustee and the Gambler

In early March we talked about the split-minded investor. The trustee, who understands the need to protect capital, because it’s hard to create. And the gambler, who’s sure the next wild idea will create a generational windfall.

If you’ve done this as long as I have you know both of those personalities are part of you. The trick is learning which one should take the wheel at any given time.

This year it’s all about the trustee. Subscribers know we have nine stocks in the Trustee Portfolio. Free readers might think nine stocks is a lot for an economy set to hit a wall at any moment. That’s partly right.

But the excessive risk-taking of the last bull market hasn’t turned to sound thinking yet. When it does, we’ll know. You can test this anytime by listening to your friends and family.

Right now, people still seem to want a hot stock idea. They whip out the Robinhood app to see if it’s available at zero commission. You’ll know it’s a bottom when they tell you stock investing is a scam.

Or, keep an eye on the more than 10,000 digital tokens tradeable through online exchanges. Pancake Coin is my favorite.

At peak insanity, the delicious token that promises to revolutionize the way we consume pancakes had a market value of ~$7 billion. Yes, you read that correctly.

Down ~97% from its high, Pancake Coin still has a market cap of $250 million. $0 seems more appropriate.

The trades that worked when fringe token traders, SPAC speculators, and house flippers had piles of capital gains don’t work today. In fact, the features of the last bull market reversed to create the opposite:

· Higher interest rates

· Tighter credit terms

· Expensive mortgages

· Limited cash for speculative startups

· Expensive energy

· High return thresholds for investors

It’s the time to own things people need. Resilient demand, profits, dividends, and low debt levels, were out of favor during the last bull market. That’s not the case today. For now, that’s where we’ll focus our attention.

Portfolio Update