When Everyone Agrees

They’re usually wrong

Paul Shemwell loves stocks.

He told the Wall Street Journal he keeps 95% of his $6.1 million net worth in the market through index funds and individual stocks… like Apple Inc (AAPL).

$6.1 million might seem like a lot of money, or nowhere near enough. It depends on your perspective. Either way, the Journal says it ranks Shemwell in the top 0.1% of retirement savers.

95% meant he had around $5.8 million in the market at the time of the article. Which left the other $305k for things like… somewhere to live, and his 2016 Infiniti.

Plus, Shemwell still had a mortgage. Meaning, he’d rather be in debt than sell stocks. That’s real conviction.

At 65-years-old, he plans to live another 30 years. If you can plan that kind of thing. His dad lived that long, and he figures he’ll do the same. He cites expected longevity as further proof he needs to stay in the market.

But his dad lived in a different time…with a different stock market. It was the post-war boom in America. Hard work and frugal living made fortune building a simple process.

It’s why the current Shemwell says he likes to “keep things simple.” To him, that means driving his almost ten-year-old car, living “below his means” and paying his credit card bill in full each month.

There’s nothing wrong with any of that. But doing what worked last century doesn’t always get the same result today. Meaning, an austere approach to spending and total conviction in the stock market might not be the slam dunk he expects.

For instance, his AAPL position gave back two years of gains recently… in a hurry. Hopefully he’s right about the always go up thing.

And Shemwell’s not alone. People today make big sacrifices to stay in the market. They defer enjoying life in some cases. The general feeling is, they’ll get more money if they wait… because stocks always go up.

The Consensus is Often Wrong

When everyone agrees on something, you might want to do the opposite.

Generals fight the last war, and people buy the last bull market. They trust it…because they watched it happen. They feel comfortable it’ll happen again. But it usually doesn’t.

Take 2010 for instance. Most people thought the market was a dangerous place for money. Buying stocks that year took real guts.

The S&P 500 Index (SPX) spent all of 2010 flopping around 1,100. That was a full 25% below its 2007 high.

For context, it meant a 2010 version of Paul Shemwell endured three full years of painful gyrations with 95% of their net worth… before seeing it finally recover about half the total loss in year four.

To put this in today’s terms, imagine logging in to see a $5.8 million portfolio earlier in January. It’s a mix of index funds, and individual stocks like Apple Inc (AAPL), about what Shemwell described to the reporter.

Then imagine watching the $5.8 million fall slowly from now until the summer of 2026…bottoming out at around ~$2.5 million.

In that case, it’s 450 days of checking on the account value, wondering if the worst is over, and surely calculating the outcome of making a rash decision. Making things worse, you’d have the occasional wicked relief rally, luring you back in to think it’s all clear.

Or, being one of those people who say they don’t watch at all. They don’t log in, they don’t even think about it. You really have to wonder how these people earned the money in the first place…

More likely, the account holder watching $5.8 million fall in half over 450 days is worried about it. And in the 2007 to 2010 period above, when things finally did turn back up it didn’t feel like a bull market.

Plus, like Captain Shemwell, most people have a job. He was a pilot, at Southwest Airlines. It’s hard to watch the market when 180 people depend on you for safety in the back of the plane.

Maybe the captain doesn’t need to watch the market… since it always goes up.

People Forget to Purpose of The Money

To be clear, we’re not giving Capt. Shemwell a hard time. He did after all disclose his net worth and personal details, including his passionate beliefs about the stock market, to a WSJ reporter. Which makes it fair game…

He seems like an interesting guy. Going on to say he starts most days with a tennis lesson, which is a great choice.

And from the picture below, we see he hits a one-handed backhand, which is the more elegant choice for returning baseline shots on your non-dominant side. (he’s apparently a lefty)

He lives in Houston, TX. If any of you know him, please forward this to him. I also hit a one-handed backhand, and would accept an invitation to play a match against the captain. Of course at my racquet club in Florida, but preferably in Houston, a city I need to re-visit.

People rarely know about the world-class art scene in Houston. From the Rothko Chapel to the gigantic Menil Collection, to the dedicated Cy Twombly gallery. You could spend two full weeks viewing art in Houston and not see it all.

And if I do haul the Yonex racquets over there, I’d do my best to nudge the captain towards living now versus holding out for more in the stock market.

Just A Little More

People often seem unable to define what “more” means. They sacrifice today for more tomorrow. And never bother to put a number on it.

$6.1 million turning to $7 or $9 million, maybe $15 million. It’s critical to think about what $15 would do that $6.1 can’t.

To be clear, we’re not anti-wealth. Not in the slightest. Owning an original Cy Twombly would be significantly more interesting than viewing his work in the Houston gallery.

At ~$25 million you could buy your neighbor’s house, doze it, and install an ivy-walled red clay tennis court where his house used to be. At ~$100 million you could hire retired Captain Shemwell to fly you around. A little more and you’d spend all your time with lawyers defending your growing empire. It keeps going.

Billionaire by birth, Daniel Breyer, candidly relays the thoughts that keep people up at night in the ranks of the ~3,000 families in the world with 10-figure-plus wealth.

“Ok, how am I being portrayed among my peers? Do they respect me? Am I as respectable as this person or this person?”

Sounds exhausting…

And it doesn’t take much self-awareness to realize more is not the problem. It’s obsession, and the thinking that goes along with it.

Obsession means focusing on something so intently, you walk right past other things without noticing.

We read books about single-minded focus. We reward it. But in the end, it’s not the way to steer a ship over the long-term. To do that, you need to see everything around you, not just the one thing you want more than any other.

High-Risk Comfort

Making things worse… we don’t like to change our minds.

We’d rather be able to say, “We all got it wrong!” Or worse, blame some other person for not protecting us from ourselves. Truth is, they probably did issue a warning, and nobody listened.

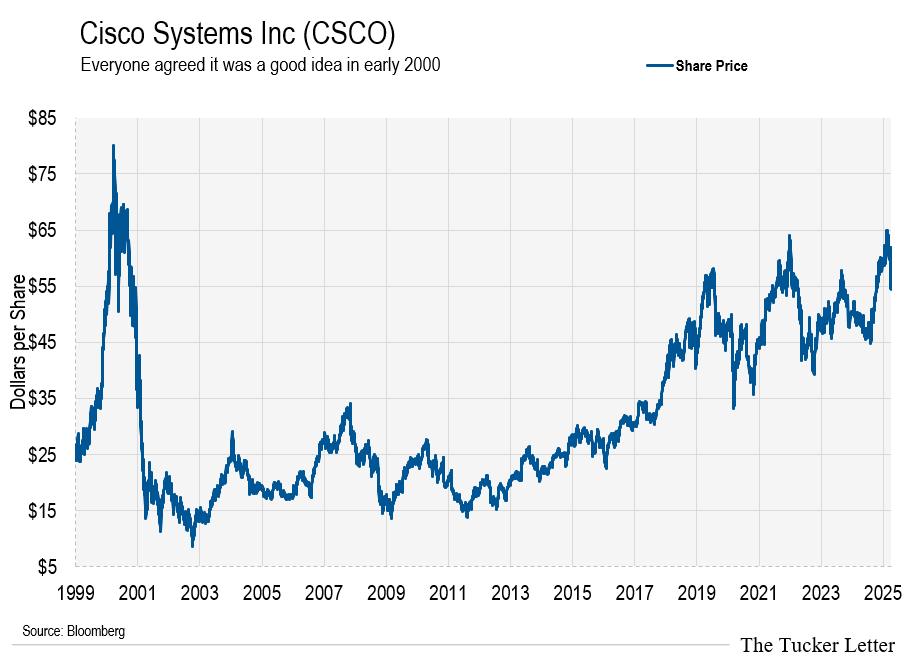

Take Cisco Systems Inc (CSCO) stock in the late 1990s. Everyone loved it. CEO John Chambers received biblical reverence when he spoke.

CSCO made routers and switches critical to connecting people to the burgeoning internet. If you’re young, try to imagine a wall-mounted phone connection as the tether to the online world. It was the stone age.

Either way, CSCO traded at ~109x times its earning power, maybe higher. And all the Captain Shemwells of the day bought it like a blue chip. 25 years later, they’re still waiting for the stock to make a new high.

CSCO makes plenty of money, it’s a good company. But today it trades at a more rational ~15 times projected earnings.

And it reminds me of the nagging question junkie stock buyers keep asking. Will NVIDIA Corp (NVDA) go back to $150.

I tell them, “Probably not” just to watch the look of horror show up on their face. But truthfully, imagine asking someone this question… it’s totally subjective.

As you’ll notice in the chart below, $150 doesn’t look like a good bet.

TTL subscribers recognize the two lines on the current NVDA chart, and know what it means when one crosses below the other…

The bigger point is, doing what worked for 15 years might not work well going forward… Worse yet, it’s tough to go against the general consensus.

Regime Change

Sometimes the people in power tell you exactly what they’ll do… and keep their promise.

Take the 2010 Washington Post essay by then Fed Chair Ben Bernanke. He explicitly told us a rising stock market and rebounding home price would make people feel comfortable getting back into the market…causing more investment, and more comfort. He called it a virtuous circle.

“[…] higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”

Ben Bernanke – Washington Post November 3, 2010

We didn’t believe him…

And the plan worked.

Fifteen years later, we don’t believe the plan laid out by the new regime.

Worse yet, the entire mainstream financial complex makes so much noise about it, we believe them over the people in charge. These squawkers have their own interests… not typically lined up with ours.

But what if this new plan does work?

I can’t find one person who thinks it will. Which tells me, it might.

Or, more importantly, betting on the plan working is lower risk than betting with the consensus.

Again, back to 2010, nobody believed the virtuous circle plan would work. Nobody.

In fact, popular opinion was expecting another financial crisis to happen any day. People wouldn’t get fooled again… they’d be ready. But it never came.

The move in 2010 was to load up on index funds, and large tech stocks. The same thing Captain Shemwell told the WSJ reporter he does now.

It’s human nature to stick with what worked… and get comfortable. When you walk into the casino for the first time, you have strict rules. After winning all night, you forget all about them and obsess over more. So much so you can’t notice changing circumstances around you.

If It Does Work…

There is no chart to illustrate the seismic shift underway right now in markets. We’ll go through some of the specifics in the portfolio review shortly.

As for the big picture, beware of the cacophony of public and private figures lampooning the new regime over its plan, and the perceived effects.

Many of the noisy headlines end up retracted or corrected days later. Meaning, they rattle the reader, inducing worry or panic, only to later be revealed incorrect.

For instance, tariffs aren’t new. We slowly learn other countries had them in place on various goods produced in the U.S. The notion that a tariff is some hostile attack is dramatic.

Further, the allegations of overreach, foolishness, general name calling, are another example of noisy static…distracting you from seeing the path ahead.

There are too many examples to name. But notice the alleged overreach in the Manhattan congestions pricing – It’s a big issue in New York right now. A $9 toll to enter the city by car on a weekday below 60th Street.

After media allegations of federal overreach, we find buried articles detailing the real facts. It is after all federal territory…since it happens on the Eisenhower Interstate System. Then we learn the wasteful transit authority depends on the federal government for a quarter of its bloated budget.

Try to loosen your grip on narratives, and zoom out. When not one person thinks the incoming regime could possibly be successful, taking the other side of that is the real low-risk bet.

15 years of palliative market management is all we know…as a society. We fixate on $150 for NVDA but forget how much reflexive value built up during the virtuous circle.

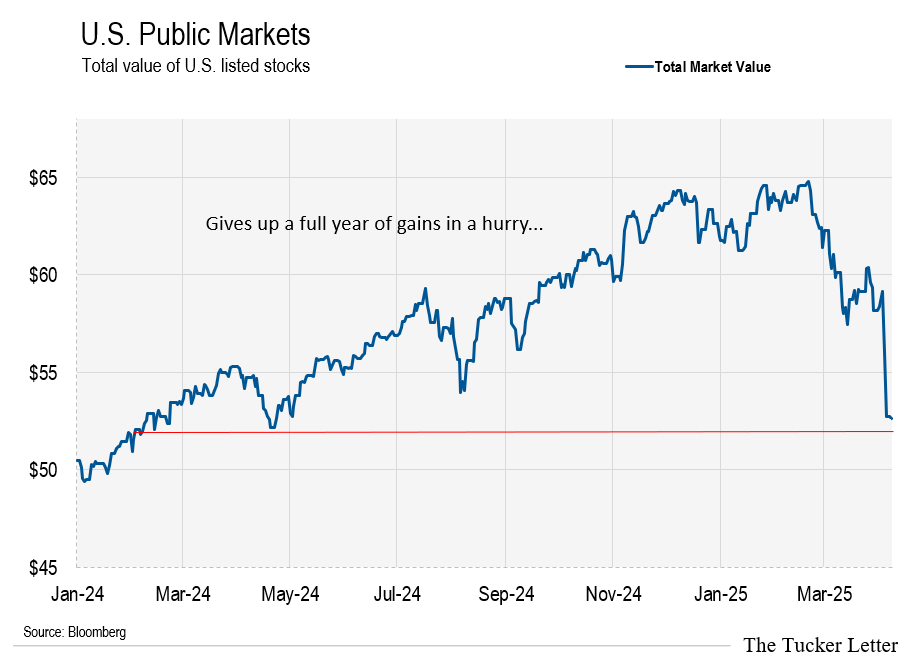

And the reminder comes when index funds lose 16 months of upticks in a few days. Don’t mistake yesterday’s snooze button for a trend change.

Gripping on to narratives can get expensive.

And while time will tell, our job is to position for what is, not what self-interested media figures tell us is important to them.

The Treasury Secretary is smart… I heard him speak in a small group last year…before the nomination. He’s polite, and I’d take him any day over a career bureaucrat.

The Commerce Secretary is aggressive. I had first hand experience with his former company… and always found it to be highly accurate, competitive, and risk-aware. I’m not sure I’d be name calling and maligning him so quickly. I’d also prefer him over an academic with loyalties to cloaked power.

And before posting a reactive comment below, consider your editor is unregistered to vote. Meaning you can elect a German Shepherd and the way we analyze what we see in front of us doesn’t change.

The Big Trend

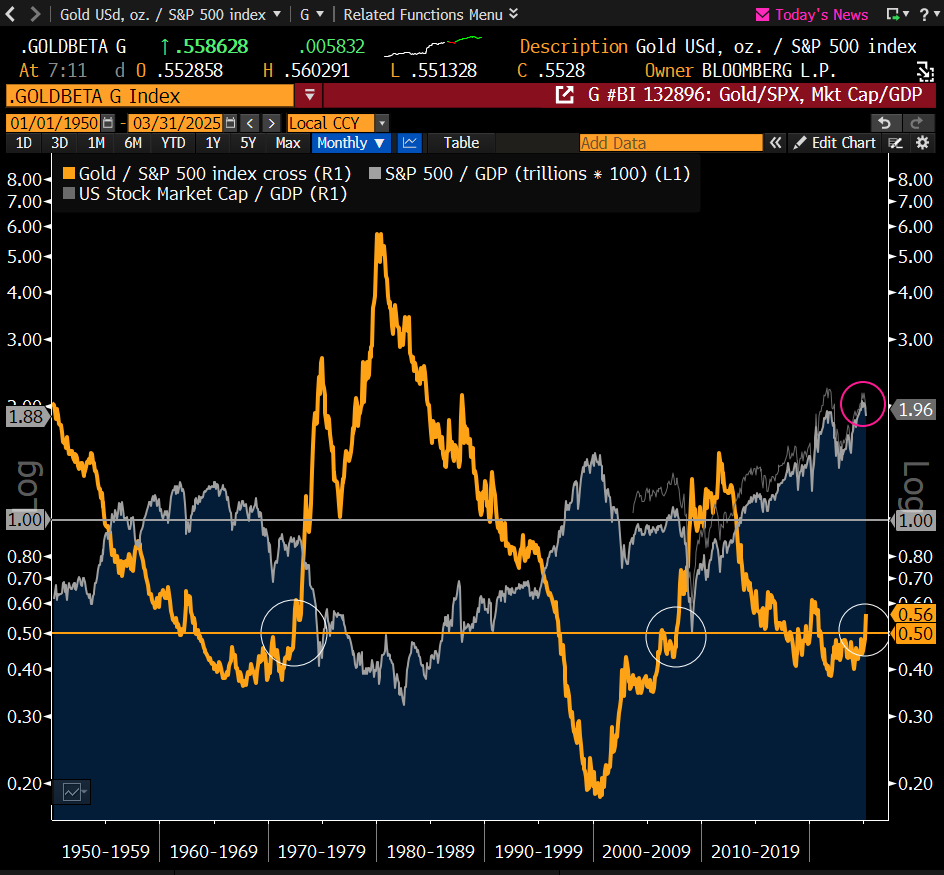

Don’t tell Captain Shemwell, but stock values are due for a pause… a big one.

This chart goes back to 1950. It compares the value of stocks to gold.

The purpose of the chart is to show when one of the two is in favor, the other out of favor.

And this is not an argument in support of gold. Instead, it’s an indicator of times when blindly throwing money at the big stock trends doesn’t work. Or, grinds sideways for several years.

In the chart, the orange line tracks gold in the ratio. The grey line stocks.

When orange rises, stocks are in go-nowhere mode. When grey rises, gold lags.

Notice we’ve just entered the period which in the past indicated a sideways grind for stocks.

Again, that does not mean run out and load up on gold. TTL readers know you can definitely have too much gold. So says the guy who wrote the book on gold. Other than chapter 24, which didn’t work out as anticipated, the book still holds up as highly accurate today.

Aside from gold, there are stocks worth owning if the new regime’s plan works. Some companies benefit, tremendously.

That’s not government graft at work either… it’s renewed economics. Economics is the science of choice when faced with evolving incentives. It’s 3-D chess. And it plays out while distracting static pollutes the airwaves.

Balancing the cost of a product or service, even better, letting the market work, changes the earning power of a company.

We’ll go through charts of most of the companies we own today. You might want to brew a second cup of coffee before we do.

Our move is to avoid the story stocks every plumber and personal trainer with a smartphone bought during the last bull market…which went on for a very long time.

Instead, we’ll own concentrated positions in companies set for a boost in earning potential.

Let’s get started.