"We Don't Fix The Price of Oranges"

Welcome to State-Controlled Capitalism

The retired CEO of a bank where I’m a stockholder told me about a run-in he had with a banking regulator. It’s enlightening. It may help make sense of today’s money troubles.

The story goes, early on as CEO he had a routine visit from Federal Reserve bank examiners.

He walked in to say hi to these civil servants. In conversation, he decided to toy with them. He asked why the Fed doesn’t fix the price of oranges. They quickly replied, “That would destroy the incentive to produce great oranges…. This is the United States, a free market, the best system in the world.” He replied, “Well then, why does the Fed fix interest rates?”

He admitted this might not have been the best way to greet visiting bank examiners. Regulators don’t take jokes well. But his point went far beyond the price of oranges.

It’s been close to 30 years since the CEO asked this question. We’re a long way from a free market. Fixing interest rates turned into a radical money experiment that now appears out of hand. His question was ahead of its time.

Capitalism Died a While Ago

My CEO friend had a special kind of genius. In addition to being book-smart, he understood why people make decisions. He noticed what influenced them, he watched how incentive motivates action.

This is what makes the free market unique, and hard to beat. Individuals decide where they’ll do business, what they’ll pay, and how they’ll use their hard-earned money. The competition forces suppliers to earn their customers. The regulator was right about one thing, the best oranges do come from a free market.

The problem is, the company producing inferior oranges goes bust. It lays off employees, sells the equipment, and leaves its facility abandoned. In a free market, a better operator would take over. The transition can be harsh. But it’s necessary, if you want excellent oranges.

The same goes for money. It’s the capital in capitalism. The best companies get funding. The bad ones go bust. We have recessions. Business slows, weaker companies can’t earn the trust of new investors, the prepared survive.

These days, the companies most connected to government survive. The masses get stimulus checks so they don’t feel the recession. In exchange, they turn their heads and ignore the vanishing free market that made it all possible.

Capitalism can be rough, painful at times, especially for the poorly capitalized. Humans generally don’t tolerate pain well. Opportunists realize this. They know we’ll slowly give up freedoms in exchange for pain relief.

We got away from the free market one choice at a time. Like a ship that changes course by a degree. At first, it’s hard to notice. Later in the journey you arrive on the wrong continent.

The system we have today is state-controlled capitalism. It’s enough to keep people believing in the idea of a free market. That’s important.

Forget Conspiracy Theories…This is Reality

Before you write this off as conspiracy, think back to the virus situation in early 2020. The U.S. stock market lost around ~35% of its equity value in about three weeks.

The chart below shows the total value of all listed U.S. stocks. Notice the peak in February 2020. Then the ~35% decline in five weeks. Then the ~38% rally within 10 weeks.

Surely you remember what happened. The entire ~$80 trillion world economy stopped on a dime. This arbitrary shutdown had factories, schools, power facilities, and systems we never think about looking for the off switch.

With the prospect of zero revenue, investors bailed. They sold stocks in mass. Bonds fell more. Each day marked a new low. Investors logically expected a downswing in the business cycle.

Then, without warning, the Federal Reserve announced a market intervention. In fact, the Fed took the unprecedented step of buying junk bonds in the open market. This means it bought the debt of companies too weak to comfortably finance themselves.

That sent the price of risky bonds higher, far higher than reasonable. Just consider the condition of the firms on the hook for these risky debts. Investors with hard-earned savings wouldn’t touch this junk. The Fed paid full price for it, creating its buying power with a few keystrokes.

Not long after, lower wage earners received a check in the mail. Then another, and another. They took to gambling in the stock market, watching television all day, and hunting for hobbies online, where germs didn’t exist. If you got caught up in the moment, you barely noticed the extreme departure from free markets.

Some people noticed, and spoke out in frustration. Howard Marks, co-founder of Oaktree Capital Group, is a legendary distressed debt investor. Earlier in his career he patiently picked through troubled assets during recessions. Those days are over.

When the Fed abruptly bought junk-rated debt during the virus, Marks said:

“What’s the Fed’s purpose in buying non-investment grade debt? Does it want to make sure all companies are able to borrow, regardless of their fundamentals? Does it want to protect bondholders from losses, and even mark-to-market declines?”

That’s not capitalism. That’s intervention, or state-controlled capitalism.

Increasingly Extreme Interventions

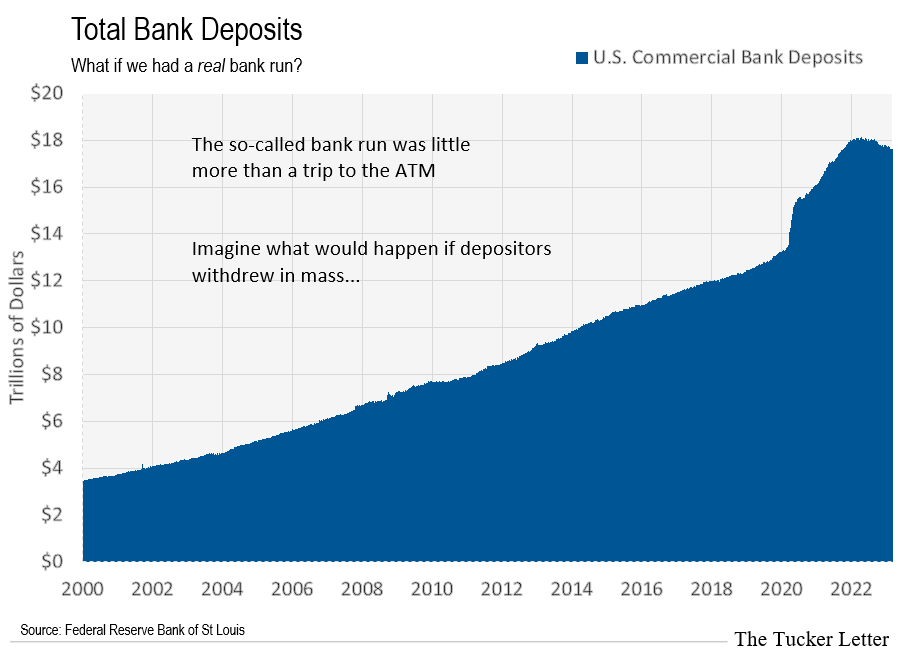

A few weeks ago, we thought all banks would fail. People shifted meager savings here and there panicked they’d lose their cash hoard.

The U.S. has more than ~$17.5 trillion in commercial bank deposits currently. Shifting a few billion barely registers in that total.

The FDIC protects depositors during a bank failure up to a cap of $250,000. Over half of deposits at U.S. banks exceed that FDIC limit according to Investopedia. 94% of depositors at Silicon Valley Bank (SVB) held more than $250,000 according to S&P.

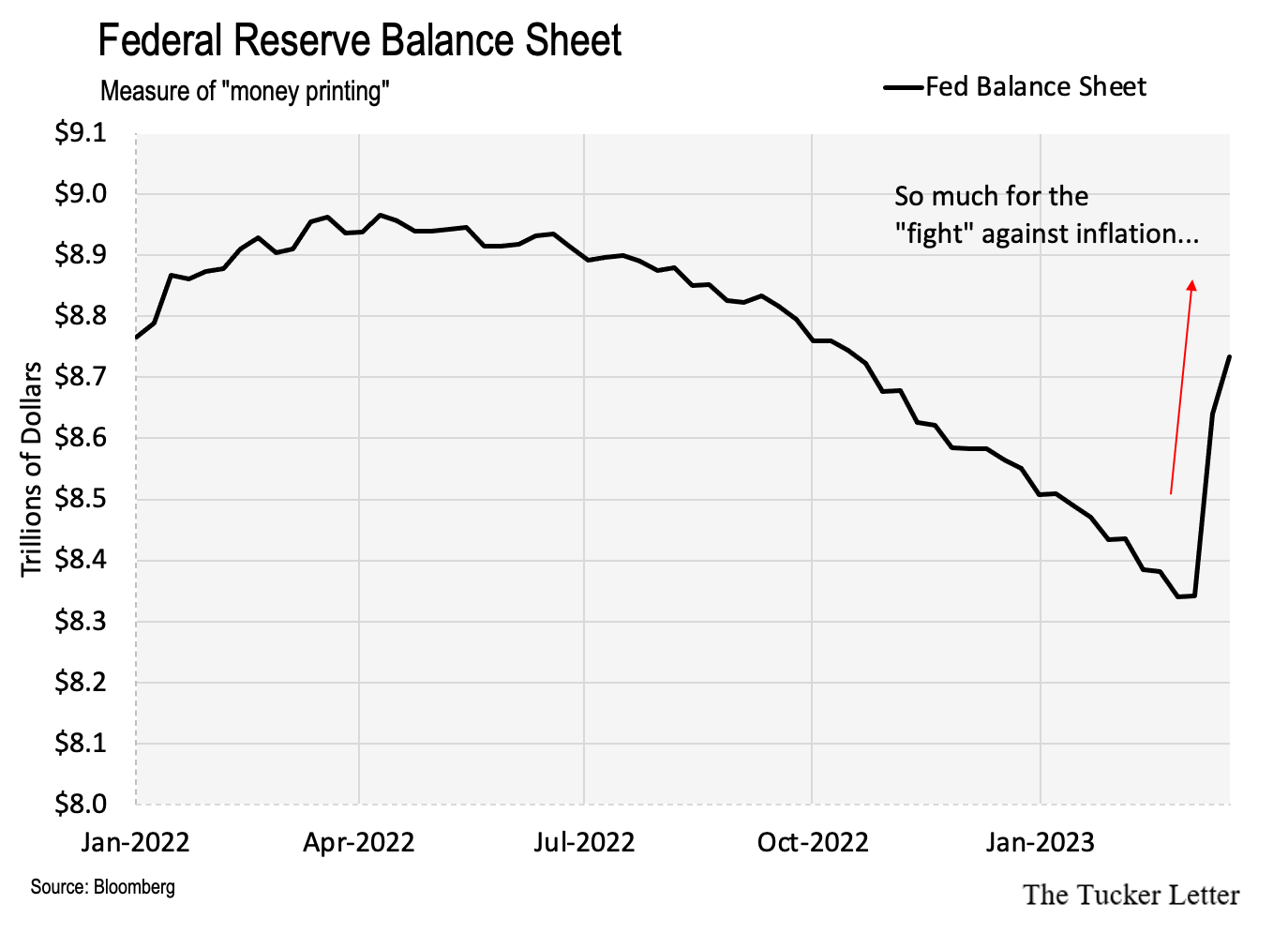

But the Fed stepped in to protect these depositors. Think about that. The Fed floods the media with its inflation-fighting war cry. People believe it. Meanwhile, it prints ~$300 billion with one keystroke when the wrong bank gets into trouble.

We don’t have an axe to grind with the Fed. In fact, we expect this, and more to come. In the end, the Fed might turn us all into billionaires.

The issue is, we have capital to manage. Capital is a relic of capitalism. Better to have it than not. If we handle it properly, it may grow faster in state-controlled capitalism than it did in the free market version.

How to Navigate State-Controlled Capitalism

It’s a little different. We’re not going to have protracted recessions the way we did last century. Remember, we’re in a perpetual boom with the occasional, brief crisis.

It’s hard to be out of the market with this type of system in place. As we build out the trustee portfolio, you’ll see my preference for stocks I can comfortably hold, even during difficult periods.

The trick here is avoiding sectors set up for a downtrend. It’s not as difficult as it sounds, don’t worry.

There are two main things I consider when making a stock investment. First, the likely direction of the sector I want to invest in. Second, the likely direction of the specific stocks I like within that sector.

I’ll give you an example below of one sector I avoided completely over the last year. You’ll see how using one simple chart warned of the downtrend in advance.

Golden Cross or Death Cross

Good investing is only part science, the rest is art. Life wouldn’t be any fun if we lived by a formula.

What we want to do is get the big picture right. It’s the 80/20 rule. The small decisions don’t matter much if you get the big ones right. As far as stock investing goes, that means staying in an uptrend, and out of a downtrend.

I’m not clairvoyant, and this is not magic. As proof, I’m occasionally wrong. While it’s just one tool in my toolbox, it’s one of the best. Here’s how it works.

Every day you can check the closing price of a stock. $5.00, 5.05, $5.03, and so on. I take the closing price of the previous 50 trading days together and get an average price. We’ll call this the 50-day average.

I do the same for the previous 200 days. The 200-day average.

I plot these two lines on a chart along with the traditional closing price you’d see in any traditional stock chart.

Let’s use the oil and gas sector as a current example. I looked at several of the stocks last week. As a comparison, I also looked at a large energy ETF. Here’s what I saw.

The first chart below is a large energy ETF, (XLE). It holds most of the major oil producers including Exxon, Chevron, Marathon, ConocoPhillips, and others. We’ll use it to see what the energy sector looked like going back to 1/1/2020.

You’ll see three lines in each of these charts. The white line marks the closing price of the stock each day. This white line is a traditional stock chart the way you’re accustomed to seeing it displayed.

Now take note of the pink and yellow lines. These lines plot the average price going back 50 days (pink) and 200 days (yellow).

When the pink line is over the yellow line, the stock is in a “Golden Cross.” This means it is in an uptrend. It may have an occasional slump, but if the pink line stays above the yellow line, the price typically recovers.

Notice in the chart of XLE, the energy ETF, the pink line moved above the yellow line to form a golden cross in December of 2020. The price of the ETF was about ~$35 at that time. Today it’s ~$80.

The pink line stayed above the yellow line the whole run from ~$35 to ~$80. In Q3 of 2021 you’ll notice it flirted with the yellow line, but turned and moved higher. The golden cross is still intact as I write.

What this chart tells us is the energy sector started looking like a good bet in December 2020. Notice the price made an initial move up a few months prior. By waiting for the golden cross, a would-be buyer increased the odds of success with the investment.

Successful investors call it, “waiting for confirmation.” It’s simply patience.

A gambler might think oil is about to run, but a trustee wants to see evidence on the chart. The trustee doesn’t mind missing out on the first $5 of the run. In this case that was $30 to $35 in late 2020. Patience paid off as that run was the real thing, carrying XLE on to ~$80. It still looks good today.

I generally don’t buy ETFs. I prefer individual stocks. Companies have features, positive and negative. I like to pick favorites. Sometimes for arbitrary reasons, but the individual chart needs to confirm the uptrend at a minimum. That means, I want to see a golden cross for the individual stock. Again, pink line over the yellow line.

Take a look at Marathon Petroleum Corp (MPC). It’s the third largest holding of the energy EFT we charted above. Only Exxon and Chevron rank larger in the ETF holdings.

MPC is smaller than the oil giants. It focuses more on refined products like gasoline and diesel. It produces these products largely in the middle of the country, close to the end-users who need them.

MPC formed a golden cross about 2-3 weeks before the ETF. Notice late 2020 the pink line moves ahead of the yellow line. This signals the golden cross.

At the time, MPC traded for around ~$33. Today it trades for ~$129. That’s a ~200% move for MPC compared to ~93% for the energy ETF over the same period.

What the chart told us is the energy sector gave a buy signal. Most energy companies ran. Better positioned companies ran more. Higher, was the general trend.

How To Stay Out of Trouble

Pink line over the yellow line signals golden cross, or a generally upward trend.

Pink line under the yellow line signals a “death cross,” or a generally lower trend.

Take the tech sector as an example. We’ll use the same time period as we did with energy, 1/1/2020 through last week.

This is a chart of Cathie Wood’s popular emerging technology ETF Ark Innovations (ARKK). It’s a widely followed way to play the technology sector, especially the high-growth, riskier portions.

Notice ARKK stayed in a golden cross during all of 2020 and half of 2021. It ran to a high of $156 in early 2021. However, it fell to just under $120 before registering a death cross (pink under yellow).

This means by watching for the death cross an investor sat through a steep decline from $156 to ~$120. By selling when the death cross emerged, the pain got worse as ARKK ran back up to ~$130. This tested the death cross through the summer of 2021. But then fell for roughly 18 months to a low of ~$30.

Noticing the death cross prevented a lot of pain. Remember, people at the time had tech fever. Only an unbiased set of eyes could see the death cross.

The same goes for tech heavyweight Alphabet Inc (GOOG). It held up longer than ARKK. It’s golden cross stayed in place until early 2022. The golden cross turned into a death cross around ~$135. Again, the high was ~$150 meaning investors battled the thinking of, “Can’t sell now, it’s down from the high.”

Those who did sell on the death cross saved themselves a lot of pain as GOOG fell over the course of the year to a low of ~$85.

Investing is a game of survival. There are times to gamble, this is not one of them.

If you stick with it long enough, you learn patience. It’s the inevitable outcome. How long it takes is different for every investor.

Introducing the Trustee Portfolio

A trustee’s job is to manage assets for the benefit of someone else. Any group, organization, or person without the capacity to manage their assets can hire one.

The job changes your thinking. Every decision keeps the beneficiaries of those assets in mind. It’s the equivalent of valet parking a Ferrari. It’s not your car. Be careful.

You can make mistakes, but you’ll need to explain what happened. Getting bored and gambling, or playing around with risky investments is not a good answer.

There’s also no need for outsized profits. Most home-run swings result in strikeouts anyway. Patient money might be boring, but over time it can grow into something substantial.

Right now, the Fed has us in a tough spot. Interest rates, inflation, bank failures, and war are all factors we need to consider. If we had a truly free market, that’s one thing. Today we have to consider what the price-fixing committee might do at each turn. But the big picture is pretty simple.

The Fed decided to inflate the debt-based monetary system for more than 20 years. Everyone including companies, individuals, pensions, loaded up with debt or they missed out. Even if you are personally debt-free, you still have a link to this system. The price of your home, car, toys, and groceries all tie back to this inflated debt money system.

As rates reach higher, the most indebted people and businesses begin to buckle. We saw it with the weakest banks. If it keeps up, you’ll see it with your weakest friends and neighbors. The ones who borrowed the most may show signs of trouble.

But it can’t last. The reason is simple. As the Fed turns their massive debt-based monetary system into a pawn shop, they’ll destroy the system. That outcome leaves them with less to control.

Think about the value of homes in your neighborhood if there are no mortgages available. Or, the value of businesses when acquirers lose access to borrowed funds. It’s the equivalent of pulling $1,000 from the ATM for a weekend trip compared to using a credit card. The former is a tight leash. The latter, loose.

That means we’ll need to be partially exposed to stocks while the Fed marches the U.S. debt-money system to the brink. Stocks might suffer, but they’ll turn on a dime at some point.

The Fed’s choice is, cripple the economy or restart the printing press. They’ll eventually choose the latter, when they do, they’ll kick off a new wave of inflation. We’ll add a stock today that should survive that wave.