They Turned us into Credit Junkies

Unintended consequences of the Fed's radical money experiment

“He glued it to the wall, didn’t even use a screw.”

That’s how Seth described the towel racks and toilet paper holders essential to any master bathroom. They fell off the wall of his master bath shortly after he moved in.

In fairness, this was a perfect transaction. Seth knew almost nothing about good home construction. The Armenian seller knew exactly how to stage a Hollywood set.

You must buy a home in the U.S. today. To be taken seriously in most circles that is. Typically, it means you also must borrow a pile of money to do it.

The Fed controls how much interest you’ll pay. Central planners realize you’ll feel good if the value of your home creeps higher, bad if it falls.

Seth stretched to buy his first home in Southern California last year. With rates higher, and the local market stalled, he’s had just over a year to get acquainted with the huge decision he made.

In the U.S., the home is much more than a place to live. It’s a thermostat connected to the American mood.

All Part of The Plan

In the old days, local banks loaned money to would be homeowners. Not too long ago, regional banks did the job. Today, it’s mega loan factories with names like Rocket Mortgage or Loan Depot. They load you up with as much debt as federal rules allow. Then they sell off the mortgages as a package to some faceless entity before the ink dries.

The point is, there’s nobody holding the other end of the mortgage. While your liability is surely someone else’s asset, it’s hard to figure out who that someone is.

The Fed likes it this way. Home prices are a key part of their twenty-year radical money experiment. The Fed itself now owns a huge slice of America’s mortgage debt.

In 2010, then Fed Chairman Benjamin Bernanke wrote an opinion piece in the Washington Post. He said exactly what he planned to do. The article came out within minutes of announcing his newest $600 billion monetary stimulus experiment. He’d buy a combination of government debt and mortgages.

$600 billion seemed like a huge amount of money at the time. Bernanke likely feared a bad response from markets. We now know the editorial piece was an honest note outlining his intentions. Financial engineering at its finest. The problem is, we didn’t take him at his word.

Here’s what he said.

“Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”

There you have it. He predicts surgically adding money to the financial system leads to a virtuous circle. Remember, that was 2010. His plan worked.

Back then, the federal debt sat at ~$2.2 trillion. He proposed adding a mere $600 billon to it. Today it’s $8.6 trillion, nearly 4-times larger.

It’s a waste of breath to argue about the dangers of that debt pile. It won’t come down in any meaningful way. Not now, not ever. The society can’t survive the sacrifices required to reduce that pile.

Remember, Bernanke’s editorial said his financial engineering would:

· Promote economic growth

· Make housing more affordable

· Encourage corporate investment

· Raise stock prices

· Boost confidence leading to higher consumer spending

If that’s what happened when Bernanke put air in the balloon, we should expect the opposite as the Fed takes air out. The opposite would be:

· Stifles economic growth

· Makes housing more expensive

· Discourages corporate investment

· Lowers stock prices

· Reduces confidence leading to lower consumer spending

The Fed’s radical era of easy credit forever changed our behavior. Like junkies, investors expect the nurse to come running at the first sign of pain.

It’s true. After two decades of financial engineering, we can barely remember the real cost of anything.

Companies rarely invested in productive long-term assets last decade. They mostly borrowed to pay dividends, boost stock prices, and whittled down assets in the process.

The same goes for consumers. Saving was a total waste of time. Live for today, take that Carnival cruise.

Problem is, consumption burns up money forever. Borrowers can’t get back the money spent on pools, jet skis, and weekends in Vegas.

Look at the bright side, everybody had fun, felt rich, and stayed distracted.

What This Means for Stocks

The economic central planners have big problems today. Much bigger than people realize.

For starters, the borrowing binge, or credit card living, caught up with them. It’s like burning the furniture to stay warm. Works great for a little while. Eventually, there’s nowhere to sit.

The U.S. sat on top of essentially a world order dominated by one major power for almost a generation. That’s a coveted spot. But it’s changing.

Nothing is permanent. No leader, country, or organization stays on top forever. You can see this throughout history. Something about the view from the top makes it hard to defend indefinitely.

Instead of a single superpower we see the world shifting into zones. I gave a speech about this in London in 2019. I had no idea 2020 would be the catalyst. That’s how predictions work. You can get the how right, but the when is tricky.

When I say “zones” it’s important to understand the meaning. The U.S. lorded over the planet for a time. Some regional powers now feel they don’t have to settle oil trades in U.S. dollars. Or, they don’t have to allow the U.S. to be the only foreign country with a military base on their sovereign dirt. Or, they can buy wheat from a cheaper source even if the U.S. formerly forbid the purchase.

The point is, as the lone superpower the U.S. forced the world to accept, store, and trade in dollars. It was a world reserve currency.

That meant our credit card lifestyle at home had real world buying power. We could print or promise our way into situations we’d never be able to save our way into. Life was good. But now the bill is past due.

That means the Fed has to firm up the dollar. It has to reign in debt, keep the system strong to maintain its influence. If foreign nations opt out of the U.S. currency in favor of other options, it’s bad for the empire.

The reason this is tough is every turn of the Fed’s ratchet puts a little pressure on people in the heartland. It has to turn the ratchet, to protect the empire. But too many turns and Seth starts squealing. He’s fairly wealthy, so he’ll be fine. But the average American is not.

When People Squeal

You may notice things tend to change when people make noise. Health mandates, restrictions, laws of all sorts, tend to change when leaders meet resistance.

So far, the Fed’s rapid rate hiking has not affected the masses. Notice the near vertical trajectory. It’s unprecedented. Almost overnight, the Fed took the cost of borrowing from nearly negative, to 5%.

5% feels like a lot for homebuyers. “Historically speaking, it’s not so high.

The issue is, people grew comfortable with rates at nothing for years. 5% feels like a lot for people like Seth who took the plunge at the tail end of the radical money experiment.

But things can get worse. A lot worse.

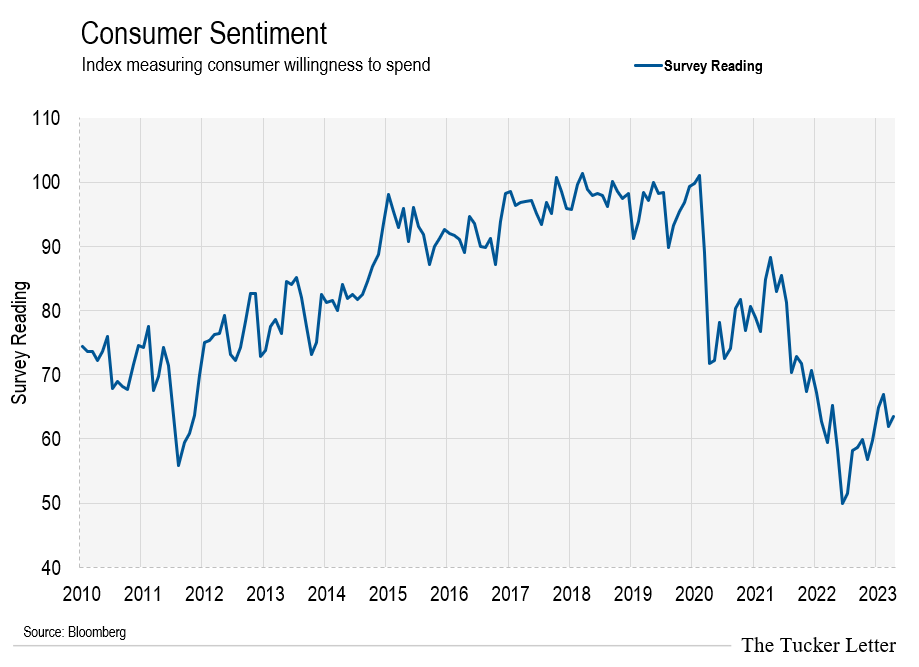

This chart tracks consumer sentiment. It’s down, but can go much lower. Keep in mind, Bernanke expected his monetary experiment to boost consumer sentiment. As the chart shows, reversing his policy by just a few turns of the ratchet sent consumer sentiment plunging.

As a reminder, total Fed borrowing topped out at ~$9 trillion in early 2022. It fell to ~$8.35 trillion by March 1, 2023 due to raising rates and curtailing bond purchases. That’s right around the time we had bank runs, credit panic, and stocks flirting with lows.

We’re back from the brink today. The Fed pumped ~$260 billion into the system to cool things down. That was just 7 weeks ago. Far too soon for the all-clear.

If the Fed keeps raising interest rates it will cripple its domestic economy and banking system. The credit junkies can’t take the pain of withdrawal.

However, if the Fed reverses course, promises more borrowing, and turns on the spigot, the dollar will tumble.

What We’ll Do to Prepare

It’s a tough forecast, but we can handle it.

This is not a time to gamble. The Fed weans us by removing the easy money from the system. That means fewer dollars chasing investment ideas. The worst ideas suffer first. Wild speculative bets don’t tend to play out well with the tide going out. There can be a winner here and there, but overall, the odds don’t match the risks.

The Trustee Portfolio has a different mandate. You only have to sacrifice once to earn and save a dollar. After that, you have to keep it.

Today that means focusing on companies not dependent on credit card living.

Several people messaged me this week referencing my comments on Bed Bath & Beyond in the March 2, 2023 issue.

I appreciate the kind words. But we’re not trying to short stocks here, or to be right with huge calls. The BBBY comments were about now being a bad time to gamble. People flooded into BBBY in the weeks before I made those comments.

From my March 2 comments to today the stock fell ~93%. It still trades for ~$0.11 as a bankrupt company. I’d suspect shareholders hold on to $0.00/sh of value after bankruptcy.

The point is, in my role as trustee, I have different motives. It’s not boring by any stretch. But we can’t depend on a squeezed consumer until the Fed reverses course and comes to the rescue. It’s hard to predict when that happens. In the meantime, we’ll get into a stock with a different source of revenue.