The Foundation of Your Money House

It’s time for an inspection

Last week I had the smallest scoop of ice cream I’ve ever seen. When the bowl hit the table, I stared in disbelief.

It was the size of a melon ball. So small, I asked the server if there’d been a mistake.

She told me unfortunately, that’s the serving size for ice cream at Miraval. However, there’s no charge for food. She suggested I order 6 scoops, which I did.

6 of these “scoops” did equal one regular scoop of ice cream. It seemed like a silly way to think about navigating a dinner menu.

There are no prices on the Miraval menu. The idea is, they want a relaxing environment for guests. Putting prices on the menu cheapens that…so they think.

But prices are an important part of a good dining experience.

For starters, the wait staff helping me last week seemed lost. They were nice people. But they didn’t feel like professionals. I had questions, they didn’t have answers.

With prices on the menu, servers tend to know their stuff. Ask where the fish swam, how the lamb should be cooked, or what to drink with the meal, they should know.

If they don’t know, they should make up an answer on the fly. There’s nothing worse than a server telling you it’s their first day, and they don’t know the answer. The uniform and nametag gave me confidence. There’s no need to disappoint me. Just make something up, be convincing, I’d probably believe it.

To curate a certain type of experience, Miraval nearly destroyed the act of dining…which should be an enjoyable transaction.

Removing the Market System

Transactional commerce gets a bad rap. But there’s something honest about it, honorable even.

If the server doesn’t benefit form a meal well-served, it won’t be. Customers complain, they call for the manager, and ask that unacceptable items come off the bill. But without prices, complaints get a smile and a nod.

Hyatt Hotel Corp. (H) developed the Miraval concept. They have three locations as far as I can tell. The $13.5 billion hotel chain thought it would offer luxury wellness to the masses. It’s a decent idea. But it’s not the real thing.

Hyatt commandeered the palatial 130yr old Wyndhurst Mansion in Lenox, MA to develop the concept. The mansion and grounds are beautiful. It built out surrounding accommodations that feel like a traditional hotel.

I went to Miraval last week to hash out an idea for a new book. The plan is to have it out by May 1. I needed a quiet place to work, with food, which isn’t easy during the holiday week as many places close.

While the book outline came together perfectly, I was ready to get back to dining with prices.

Impossible to Predict

That’ll be my first and last visit to an all-inclusive hotel. It’s not for me.

But it is a reminder that prices, risk, and free market business transactions create the best experiences. We’re a long way from that now in the U.S. market.

People still talk about the free-market system. They tell me about rising prices, employment issues, and almost everyone I encounter predicts an impending market crash.

I like to know what non-professionals investors think. Workers who should be savers, and by no fault of their own, are now speculators. While they don’t know it, I’m surveying market sentiment as I listen to them. Right now, they mostly expect a market crash.

It’s impossible to predict a market crash in a controlled system. During capitalism, we’d survey retail stores, count traffic, and monitor indicators like fuel demand or package delivery data. Those days are over.

What matters now is the next move by the central planning committee. They have us hooked on debt, leverage, and the idea of flipping something for a quick profit.

There’s nothing wrong with making a quick profit, but this gets us confused. We end up so focused on the issue of the day we forget the big picture.

There are two reasons to be skeptical of your neighbor who seems sure there’s a market crash around the corner. First, they don’t have a good track record of predicting things. In fact, they tend to remain skeptical until the late innings of a trend. Once they feel comfortable, they pile in. Bad strategy…

The more important reason to be skeptical of a crash is the U.S. system can’t handle it. When a system is centrally controlled, it either grows, or it collapses. There’s no slow, natural contraction.

What this means is watching recession indicators that worked in the 1970s or 1980s is useless. The only thing to watch now is the Fed. We should watch what the Fed watches.

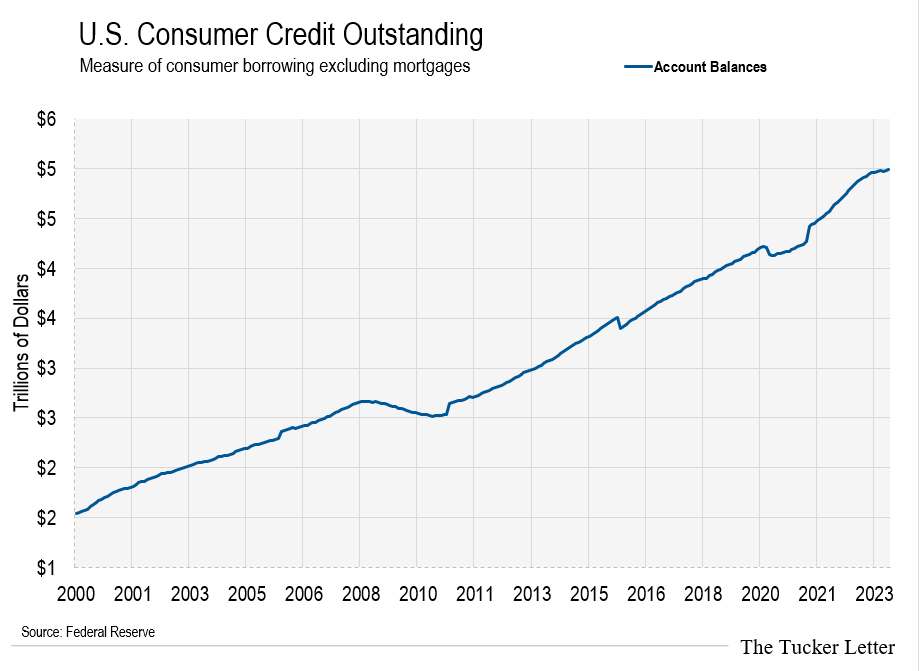

Consumer Debt at Maximum Levels

So far, things seem fine. People talk about pain, but I don’t see it.

Last weekend the President’s lead economic advisor went around the weekend news shows bragging about the health of the economy. He said we’re in, “good shape.” He cited consumer debt levels returning to normal.

What he meant was the rate of consumer debt growth. Skeptical of his comments, I looked into the total consumer debt pile. As expected, there’s nothing normal about it. It keeps growing.

And Bernstein, Biden’s advisor, is a smart guy. He realizes without more debt, the whole thing stops.

Without more borrowing, there’s no more spending. Without more buying, asset prices decline. This system overnight goes from perma-boom to collapse. And that can’t happen.

The Fed’s alleged fight against inflation is not what it appears. Sure, it needs to rein in excessive inflation. But don’t be fooled, the Fed needs inflation. The U.S. government needs it too.

Notice Bernstein also cites, “rising after-tax income” in the Bloomberg article above. He knows people need more income to take on and service more debt.

The U.S. government also needs more income to support more borrowing. People talk about the Fed “printing money” to finance government largesse. It can do that as long as government income rises.

We’ll get a look at 2023 tax receipts soon. Capital gains surely lagged the 2021 and 2022 extremes. If tax receipts come in weak, watch out.

With consumers and their government leveraged to the max, the system needs to keep expanding to avoid collapse.

Brief Panics…Not Recessions

Think back to the virus crash of March 2020. The stock market lost 1/3rd of its value in roughly three weeks.

That means before you realized you wouldn’t leave the house for the rest of the year, ~$13 trillion of market value vanished.

Four years later, the value of the U.S. stock market is ~50% larger than its pre-virus peak.

The point is, trading downturns is not easy in a centrally controlled system.

Recessions were obvious in advance during capitalism. We’d see things slow down. You’d notice the banks tighten up, less lending, slower foot traffic. People keep looking to those indicators now. But they don’t work the same way in a centrally controlled economy.

I know wealthy people bent on the idea the market should crash. They read information supporting this view. They buy puts on the indexes until they generate losses so large they begin selling other assets to keep the bets going. They turn this junky behavior into a battle of the egos.

It’s unwise. The Fed has more tools than you. You might be smarter, a better small business operator, and certainly tougher, but you’re outgunned.

Shaky Foundation

Even if you get the short trade right, you’ll miss on the timing.

It’s a matter of statistical odds. People tend to run out of capital before the flush happens. When it does, you’re left watching it on CNBC. You tell people about the bet you had last year, which was early. Early equals wrong.

Before placing a bet on the short term direction of the market, ask yourself if you want to earn that money again...the hard way.

People tend to fixate on winning. They dream about it. They rarely think about the cost.

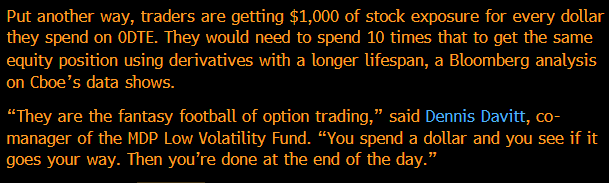

Take for instance the booming zero-day option trend. “Zero-day” means you buy an option on the outcome of today’s price action. And it’s a huge trend.

This reminds me of stories from the 1920s. Degenerates stood outside bucket shops betting on every kind of outcome…until they didn’t have the dollar needed to place the bet. That’s when the betting stops.

The trend of betting on today’s price action is so big CBOE Global estimates ~$520 million per day of premiums paid to bet on the S&P 500 Index alone. Gamblers get 10-times the action they’d get for a longer bet. Longer means a month these days.

Fantasy football is right…

Obviously, if you’re a professional options trader running finely-tuned risk models, you know what to do with these bets. But that’s not most people.

In fact, most people forget all about the risk modeling. They dream about the big win.

Instead of dreaming about the big win, let’s play the big picture. We know the market looks unhealthy. Professionals sit glued to the TV when anyone from the Fed shows up at a microphone. Without more debt, more liquidity, most trades don’t work.

Instead of betting $1 for $1,000 of action by 4:00 PM today, let’s get under the house and have a look at the foundation. It’s the exact opposite behavior…and it’s the perfect time to do it.

Easier…With A Strong Foundation

The Trustee Portfolio is a look at what I’m doing in the role of trustee. I manage the equity portion of assets held in trust. I can be fired, and might be if I fail to act in the best interest of the beneficiaries.

It means I have to justify the decisions I make. I don’t need massive gains. I don’t need to sit in all Treasury bills either. I need to expose the portfolio to growth, and survive a quick market swoon.

Subscribers know how this works. I wait until the following day to act on any recommendation, giving them a full day advance on me.

If you’re new, there are three ways to read The Tucker Letter. Choose the way that’s right for you…

1. Free – Enjoy a large section of the general commentary up to the paywall

2. Subscriber – Enjoy the full article including closing notes and portfolio access

3. Founder – All of the above including quarterly notes with a deeper dive

This week, we’ll start the year with a foundation check.

Our Stable Foundation