How The Fed Ruined Your House

How The Fed Ruined Your House

Why personal space matters

The house you choose to live in says a lot about you. In America these days, it doesn’t say much.

That’s not the homeowner’s fault. Not entirely at least. The Fed gave them an incentive to act, and they did.

For most of the 20th century a house was a place to live. Sure, you could sell it when you moved, pocketing a small gain at times. But it was a home first, and an asset second. It was rarely an investment.

That all changed around 2000. About the same time the Fed embarked on a radical money experiment. The way it looks now, capitalism in the 20th century proved too hard to control. With the big evil communist enemy slayed, it was time for a new era. The appreciating value of the family home would set the mood of the inhabitants.

With free market capitalism in the rearview mirror, we have something slightly different today. It’s a centrally controlled economy inspired by capitalism.

In this new type of hybrid system, the American home must appear valuable. Not excessively so, or emerging adults won’t see a way to play along. Ideally, the value ticks up in a steady way. Almost in a centrally controlled way.

The home is often the family’s largest financial asset. Never mind the cluster of first, second, and even reverse mortgages dangling from the title. If the perceived value keeps climbing, the residents keep borrowing, spending, and ignoring most every flashing red economic warning sign they’d otherwise notice.

“…central bank models have long incorporated the wealth effect of house prices and other assets on spending…” Janet Yellen

During capitalism, a prospective homeowner saved up a down payment. This was ~20% of the purchase price. Facing the prospect of double-digit mortgage rates in the late 1970s, some people saved up ~50% or more of the purchase price.

Plus, the local bank wrote the mortgage. That meant keeping a good name around town. Foreclosure was serious, and personal. People on both sides of the table thought carefully before signing on the dotted line.

Centrally controlled capitalism is different. You might only need 3% down, sometimes nothing at all. And forget about the local bank. Over email, someone at Rocket Mortgage, Loan Depot, or Gateway Capital who advertises a “Same Day” mortgage, takes care of the funding.

Twenty-five years into this experiment, residential real estate is sacrosanct. Don’t dare tell someone a home is an expense, a consumption item, or worst of all, a depreciating asset.

Like a carefully curated wristwatch, a home can and should express the personality of the owner, regardless of costs. When it does that, the owner tends to be a happier resident.

Designed With Purpose

After World War II the U.S. had a major housing shortage. Troops returned home ready to settle in, raise families, and get back to regular life.

The war-time production boom changed supply lines forever. Post-war capacity of steel, concrete, and other durable building materials set the stage for a new era of homes. Veterans turned into skilled laborers. The combination created a unique moment in architecture.

In simple terms, architecture is marriage of form and space. Form, as the materials. Space, as how you use the material within a unique setting.

Properly classified as an art form, the profession requires both sides of the brain. Left brain for learning the scientific limits of materials. Right brain for where to put them.

In 1945, Arts & Architecture magazine recognized a unique opportunity around surging demand for U.S. housing. It commissioned 36 homes from notable architects of the day. The instructions were:

“…using, as far as is practicable, many war-born techniques and materials best suited to the expression of man’s life in the modern world.”

One by one, these case study houses popped up. Most dotted the expanding landscape of Los Angeles. This coffee table book shows pictures, plans, and details from the designs.

While the images appear stunning, expensive, and out-of-reach, keep in mind the primary mandate of the project. The home had to be practical, affordable, and take advantage of cheap, abundant materials.

This type of design home is not for everyone. Broad swaths of the U.S. population choose utilitarian homes.

Where I grew up, poor people lived in wood houses. Wealthy people used brick. The very wealthy used columns on the front of the brick. Giant, traditional boxes, with manicured hedges projected an image of durable wealth. The one person with a design home, a tobacco industry executive, was weird.

For some reason, bigger is better in America. Design, functionality, and feeling take a backseat. And during capitalism, the people with capital had the biggest houses. In our modern era, everyone has a big house.

The Cavernous American Box

Until the early 2000s, being a real estate agent was nothing special. For decades, home prices barely kept pace with inflation. Falling mortgage rates changed that.

As interest rates fell, mortgages ate less of the monthly budget. That meant with the same monthly payment, a homebuyer got more house.

Getting more of something resonates with Americans. Visit a Sam’s Club or Costco and watch people shop. They load up on twice what they need if the price feels like a bargain.

This is the same sales technique used by Little Caesar’s Pizza. Give the customer two low-quality pizzas and they feel better about the transaction. They feel so good they overlook stomach cramps. They think only a fool would pay top dollar for one amazing pizza.

And the feeling of getting a bigger house overrides the vapid experience of living inside the low-quality box.

Today, the builder controls the homebuilding process. While that might sound normal, it’s not.

If Arts & Architecture magazine asked builders to design case study homes, they’d get something like this.

To the builder, cost per foot, profit, and compliance with local codes matter most…in that order. Fitting the most square-footage on the lot is the primary goal.

The homes of the post-war era often had concrete walls, large glass windows, terrazzo floors, and room for elegant landscaping.

Homes today have customized options with kitschy names denoting unique features like one bay window, or an alternative shade of brown paint.

My lawyer wanted to tear down his older home and custom-build a new one, with a particular style. He called half-a-dozen builders. Not one would take the job. The issue, too small. Finally, a builder told him the reason, “I can’t make money building that…”

He reluctantly agreed to a gigantic ~6,000-foot home. When I checked in on him, he said, “we’re getting used to it.” His wife and daughter have plenty of room. Everyone has plenty of room. Too much room.

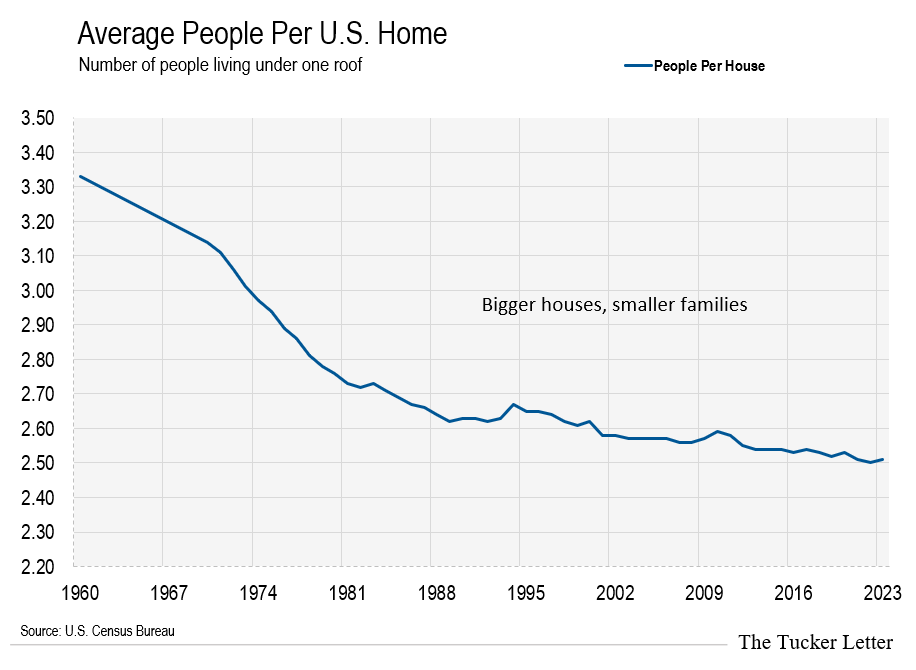

The median size of the American home is ~800 feet larger today than in 1980. It’s twice the size of 1945.

Meanwhile, the cavernous boxes we call home feel like empty gymnasiums.

Builders rarely consider natural light, landscape, orientation of the structure, or any unique feature of the subject property. This is what architects do… but the builder often declines work tied to an architect.

The reason, too complicated. And they’re right.

The Fed’s experiment with persistently rising home values changed the work culture. Fix-n-flip TV shows replaced the craftsmen of This Old House. New paint, mulch, and ceiling fans with remote controls give buyers a showroom feeling. The mortgage broker helped with the rest.

Bigger Isn’t Better

I live in a ~1,700-foot home. It’s two unique structures. One old, one new, connected by a covered deck made from Brazilian Ipe.

The two structures separate parts of my life. I sleep in one, and work in the other. For me, it’s perfect.

When people visit, they don’t say much on entry. It looks nice, pristine, but understated from the front. After walking around, they always stop to say how good the property feels. And I agree.

It’s a writer’s paradise, a unique fingerprint, and an expression of the owner. And while expensive, it’s a fraction of what some of my friends pay to live in LED-lit boxes that feel like a hospital surgery theatre.

While I understand, and appreciate great architecture, I’m not an architect. I got lucky with my home. The right architect, seller, and market opportunity showed up unexpectedly. I jumped on it.

Creating a unique home space is increasingly difficult…almost impossible in most places. Cost is less of an issue. It’s the lack of craftsmen. The few that exist have backlogs up to a year. No builder will deal with that type of delay. The demand for plywood boxes is too strong. So are the profits.

And the Fed wants it that way. People feel rich with a big mortgaged box. If they feel rich, they behave better. The last thing you want is people feeling bamboozled by reckless monetary policy. They might revolt.

But bigger homes feel lonely, lack expression, and cost a fortune to maintain. While the Fed makes more space possible, we pay the price. Gigantic boxes, heaping piles of debt, and hoping to speculate on the next hot stock idea takes a toll on society.

The big box housing trend won’t slow down, nor should it. The Fed’s plan works, and we benefit from it. Those giant boxes need air conditioning, and other services. Today we’ll add a stock to the Trustee Portfolio that benefits from every square foot of added space.

As for me, I’ll stay behind the 6-foot concrete wall my architect designed. It’s nice in here, and the neighbors have no idea why.

In time, I’d like to build a case study house. The antithesis of the modern cavernous box. I’m willing to lose money doing it. I want to see how people interact in the space, how they feel, and what they think. If you’re interested in this idea, please leave a comment.

Buying Into a Family Business

To profit from the cavernous box trend we’ll buy the largest distributor of HVAC systems in the Americas.

Keep reading with a 7-day free trial

Subscribe to The Tucker Letter to keep reading this post and get 7 days of free access to the full post archives.