Fallen Angels

What happens when debt gets too heavy

Nobody wants to be a former billionaire…

Take Charif Souki for example. He is the American dream in human form.

Sharp, focused, and not afraid of hard work, he rose to the top on his own power.

Thirty years ago he owned an Italian restaurant in the Brentwood neighborhood of West L.A. It was coincidentally where Nicole Simpson ate her last meal. She and O.J. loved the place. Everyone loved it, and everyone loved Charif.

The Simpson media frenzy took all the fun out of the restaurant business. Charif was a showman. He needed a new stage. So, he made the unlikely transition to…energy stock promoter.

It worked. Great restaurants often have a charismatic owner. He knew how to make the customer feel special, and most importantly, how to make a story sound amazing. Turns out, those skills also play well with stockholders.

His first big pitch involved importing cheap, plentiful natural gas from the Middle East. The concept, known as liquified natural gas or LNG, was new at the time. It’s a process that chills gas to negative 260 degrees turning it to liquid. Then pumps it onto a giant ship, make the trek to Houston, and unload it for use in the U.S. market.

He raised a few billion to make this big idea a reality. The complex facility opened just about the time the U.S. shale boom kicked off. That sent gas prices tumbling. It meant Charif had plenty of imported gas for a market now flooded with gas.

A quick thinker, he pitched a plan to reverse the process. With a fresh $20 billion from investors, he’d switch from importing to exporting…in a hurry.

The plan worked, and it made Charif Souki the highest paid public company executive in 2013 taking home $142 million.

Add to that, stock sales, incentive plans, and other deals, and the cash piled up quickly. But it wasn’t enough.

A Billion Wasn’t Enough

When activist investor Carl Icahn dethroned him in late 2015, Charif quickly launched a rival company.

That new firm, Tellurian (TELL), gave him another ~$650 million worth of stock at its peak. However, the value of his stake today is ~$1.52 million…according to Bloomberg. If correct, it’s a 99.8% decline.

That steep decline is not all due to a poor company performance. Bloomberg also shows lenders sold as much as ~$37 million worth of TELL shares pledged against personal loans.

And when we say sell, we mean hammer it into the ground mercilessly.

Charif might not have caused the share decline, but he certainly didn’t help it.

He did what most wealthy executives do these days. He borrowed against his stock. That only works if the share price keeps rising.

What starts out as a tempting pitch, occasionally ends in a nightmare.

I’ve heard the pitch myself. It goes like this.

“Don’t sell your shares. We’ll give you a massive loan using your shares as collateral. We’ll only charge you 0.80% interest… Your shares keep going up in value. This way, you get to spend the money and keep the stock. It’s the best of both worlds.”

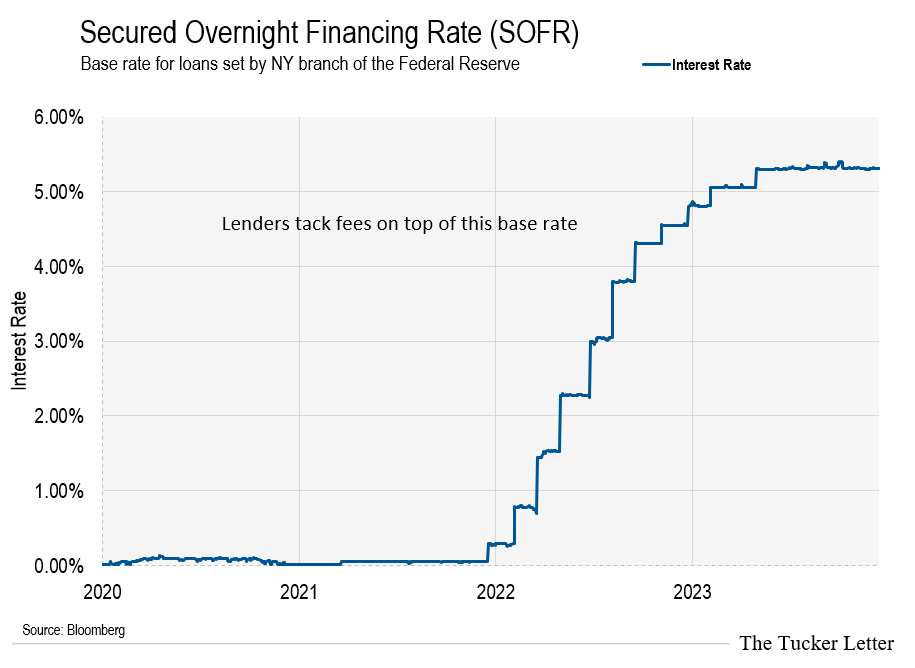

Here’s the fine print. That 0.80% interest rate is on top of SOFR. That’s the Fed’s Secure Overnight Funding Rate. It replaced LIBOR as the base rate for big loans.

SOFR sat around 0% for years. Then it went up…way up. Now that 0.80% loan costs ~6.1%.

Pretend you’re the founder of a gas company. You have stock worth ~$650 million at its peak. The bank offers you ~$50 million at an interest rate of 0.80%. Your stock secures the loan. Seems like a smart way to free up spending money.

Then a few inconvenient things happen…in this sequence:

Fed boosts rates sending the annual interest expense on your loan from $400,000 to $3,050,000

Your stock falls dramatically causing the bank to ask for more collateral

The value of things you bought with the $50 mil goes down to $35 mil

This scenario is a trifecta of pain. You keep the bank at bay for weeks, maybe months. You call in favors, bide time. Then the worst happens. The bank tells you they decided to sell your stock.

You’re left with 99.8% less stock. That’s almost worse than losing 100%.

Next, they sell your Aspen ranch. Then your competition sailing team, including boat and crew. While it might not be a wipeout, it sure feels like it.

Rarely Satisfied

The energy business was good to Charif. He was a pioneer in the gas export business. He made a lot of money, and he deserved the success.

Not content to relax at his ranch in Aspen, CO, Charif got back in the game. He co-founded a new gas company, and borrowed against the stock. As the stock fell, his problems compounded.

When people make money slow and steady, they have better odds of keeping it. A fast fortune is more dangerous. That might be life’s revenge.

But Charif isn’t the only one…

44-year-old Mat Ishbia borrowed against his shares of mortgage giant UWM Holdings (UWM) to buy the Phoenix Suns. Bloomberg shows his net worth as ~$6.3 billion.

Oracle Chairman Larry Ellison reportedly avoided selling shares by borrowing against them. He owns 98% of the Hawaiian island Lanai, a chunk of the Indian Wells, CA tennis venue, Nobu restaurants, and an array of assets so vast Bloomberg estimates a net worth of ~$129 billion.

Elon Musk does the same. And the list goes on and on.

In 2022, a Morgan Stanley employee told me I should consider this borrowing scheme. He suggested, “free up some of that dormant stock value.” While I probably could have sold some at the time, I knew better than to borrow against it.

And not because I’m smarter than any of these other people. Instead, I know from experience what happens when loans come due. It’s unpleasant, and the call always comes at the wrong time.

I’m starting to think I’m the only one who knows that feeling. The entire western financial system has an eerie comfort with debt. It’s as if only a rogue few have to deal with the repo man.

For the majority, it’s borrow to the max. If there’s a problem, the Fed has your back.

$300 Trillion of Debt

Believe it or not, the national debt is not the big problem today.

While U.S. debt doubles under every 8-year presidential term, it barely makes up ~10% of world debt.

Between tax revenue and printed Fed dollars, the Treasury so far has no trouble servicing its growing debt pile.

These days, private debt piled onto a stalled economy is a bigger problem than government debt.

Think back to Charif Souki. It wasn’t necessarily the debt that got him, it was the inability to service it.

The most recent tally of world debt I found is two years old. It hit ~$305 trillion in Q1 of 2022. I’m sure it’s higher now. Nobody takes the time to keep track. Not even Bloomberg.

For the past thirty years, we’ve watched central planners fix interest rates, and shape our overall mood about the markets. We call it a free market, while it’s anything but.

Take for instance the number of public companies trading on U.S. exchanges. In 1996 there were ~8,090. As of June 2023, there were ~4,266 according to the Kogod School of Business at American University.

Over those nearly thirty years, public equities ended up in private hands.

Meanwhile, McKinsey notes private assets under management of ~$13.1 trillion in mid-2023. Bloomberg says another ~$3.6 trillion of dry cash stands idle looking for deals.

Private equity can be a soulless owner.

I had some specialized plumbing work done last year. The master plumber wanted my opinion on selling his firm to private equity. He started the company six months prior. The offer was ~$500k for the business if he stayed around to run it. I advised he take the deal, but never heard if he did or not.

How Private Equity Works

Private equity works like this. Wealthy investors put money into a partnership as limited partners, or LPs. A group of spreadsheet experts wearing fleece vests and khakis corral the money as general partners, or GPs. The GPs have the task of finding target companies to buy.

Take the plumber’s business for example. The spreadsheet warriors might figure he earns ~$100k net in his first year. They’d pay him ~$500k. Then saddle the business with ~$1 million of debt. Then issue themselves a dividend of $500k and use the other $500k to fund growth.

All the while, cracking the whip on the plumber. The trick is, tie up half of his $500k with performance metrics. He only gets the second half if the business doubles, or something like that.

Meanwhile, the cadre of prep school executives heads over to the next pluming firm. They’ll roll up 20 of them if possible. They don’t know anything about plumbing beyond how to flush a toilet.

The goal is, increase scale through acquisition. Then drive down costs. After a few years, sell to another larger private equity firm, or take it public.

The problem is, public markets only support the best of these types of listings. With the number of public firms falling, private equity needs an exit.

Most private equity funds have a 7-year lifespan. Investors enter the fund with the understanding that by year seven the companies bought by the GP will mature, be sold, and result in cash distributions sufficient to repay the investment plus profit. That’s not happening as planned.

Enter Private Credit

The pleated khaki army has a solution for the private equity problem they created… it’s called, private credit.

Last week I went to a small conference in New York to hear about it firsthand. Some of the top executives in this bourgeoning industry spent four hours telling me the same thing.

Private credit is safe

We have not been through a full credit cycle (meaning where a wave of bad deals go bust)

There will be huge blow ups but, “not from our firm”

Private credit returns are better than private equity when adjusted for volatility

Private equity returns could be far lower than expected

One by one… they all said the same thing. Even this guy, Michael Gatto, who is an exceptional lender.

While you may find his book extremely boring, it is packed with valuable information. I talks about a company I worked for 20 years ago got into so much trouble with its debt, there’s an entire section devoted to it.

Mr. Gatto shares the sentiment of his colleagues. There will be problems, but not from his firm…which does better homework. Maybe he’s right.

This is what the private credit industry looks like in chart form. What started as a niche ~$500 billion industry ten years ago, now tops ~$1.7 trillion.

Everyone on the stage points to the ~$500 billion of fresh capital sitting on the books as proof there is no bubble.

I tend to agree. This isn’t a typical asset bubble situation, yet. But there is a problem…

Simple Analysis is Usually Most Accurate

For 25 years I’ve struggled to get along with the fleece vest crowd. I grew up with these people… they didn’t like me then; they don’t like me now.

The problem was, I didn’t play lacrosse all summer, or learn how to sail. I worked…in a warehouse, on a delivery truck, and then on a furniture showroom floor. I’m writing a new book with stories from this portion of life. We’ll talk about that later in the year.

The point is, I had a different perspective. They thought about spreadsheets, math, and social connections. I thought about the warehouse, the trucks, and the commission I earned selling furniture. Each summer I learned about a new part of that business. It forever shaped how I see the business world.

The problem with private equity plumbers, electricians, spray techs, and so on, is they don’t know how the end product works. Or, why someone buys it. Or better yet, why they might buy from the competitor.

They know how to drive down costs, fire smart people that cost too much, and make a product cheaper. But they don’t know how business works. They’ll tell me I’m out of touch… I’ll let them prove it during the back half of a credit cycle. That’s industry lingo for a recession.

And that’s coming. The reason the private credit industry tripled is it solves the private equity problem…temporarily.

Act III of The Managed Economy

There’s a pattern to this. The way I see it, it’s act three of a forty year play.

In the 1980s, Michael Milken pioneered an issuance market for junk debt. Before that companies needed a strong rating to issue debt. He found a way to issue junk. That eventually triggered a problem…but it took a full credit cycle.

The 1990s saw creation of the CLO or collateralized loan obligation. This was banks irritated they couldn’t get a slice of the junk issuance market a decade prior. By pooling loans into huge packages, they had a way to issue debt, and get rid of it. That wasn’t a problem for a decade or so…eventually it created bad incentives. Then we had a big problem in the mid-2000s.

Now we have private credit. Private equity wasn’t so large twenty years ago. It was far more targeted in its approach. Sure, there were firms, my uncle ran one of them. But they weren’t out buying local plumbing companies.

With the rise in private equity the need for a friendly credit product emerged. Private credit solves a problem for private equity. And for now, it won’t matter. But eventually, it will. And when it does, the Fed stands ready to help.

Never forget what Chairman Powell did before taking the driver’s seat at the Fed. His entire career centered around private equity, mostly at Carlyle Group…one of the most dominant firms in the business. He won’t forget where he came from. And we shouldn’t either.

Portfolio Update - When The Facts Change…We Change

In Q4 last year I started buying bitcoin, personally. It had nothing to do with any reason you’d expect.

What happened was, I looked around and didn’t see any jokers. The apes on boats, the loud and proud token people… all gone.

I read a few books about the 2021 boom and bust. I had experience with Bitcoin back to the first time I heard about it in 2009 at less than $10. I very much understood the technology, as you can see in chapter 17 of my book.

What happened last year looked to me like a shift in ownership. With the barking clowns gone, real money stepped in. I watched the chart for several weeks. It kept moving in a way that told me it wanted to go to a new high, with new buyers.

Then I added it to the Trustee Portfolio at the first of the year. I waited because I couldn’t figure out the best way to buy it for the trust. Personally, I used Fidelity’s platform, then Greyscale (GBTC), and toyed with cold storage options…none of which appealed to me. This was before the ETF approval.

When I added it at New Years, I couldn’t believe the comments. Upwards of 40 comments, mostly negative. Since then, it’s up ~70%.

This chart was in an issue after we took the position. I thought it might be useful to reflect on what got us into the position….and compare it to that happened in the following weeks.

Remember, the issue was about the high cost of being unable to change your mind when you discover new information.

That said, I’m still not sure people understand my take on this. The rough value of all Bitcoin ever created, at its limit, is around ~$1.5 trillion using today’s price.

The value of all the gold ever mined is around ~$15 trillion today.

Before you jump to conclusions, run back the issues where we added Bitcoin to the portfolio. We never alleged the two assets were the same. As proof, we own both. For now, we will continue to own both.

However, ~$100k bitcoin would be about ~$2.1 trillion or ~15% of gold’s value. That doesn’t seem crazy.

It’s not the ~70% we’re up in 10 weeks that matters. The logic that got us there is far more important.

This is a case where we watched a shift in ownership, a rotation.

Just like I don’t expect to use gold for groceries, I don’t care about the teachings of Bitcoin evangelicals. If you’re at a certain level of wealth, you might simply want to own a little bit of both.