Beware of a Weak Handshake

The true cost of Zoom meetings

We showed up to a nearly empty conference room. There weren’t more than a dozen other investors attending the meeting in person.

It was the last annual meeting of Jefferson-Pilot Financial (JP), the first stock I ever owned.

My grandfather also owned shares of JP. He thought the life insurance business was amazing. Customers pay premiums every year in exchange for a fixed payout at death.

Life insurance buyers are generally responsible people. They tend to live for a while. That means the cash from premium payments piles up on the company’s books. It invests that money during the customer’s life and keeps the profit. The industry calls this big pile of idle cash the “free float.”

But how each company invests the float is up to its management. Results vary wildly. Meeting these decision-makers in person is one of the only ways to gauge how they might put the money to work.

Attending the JP annual meeting was my grandfather’s idea. He called me in the spring of 2005 to talk about it. The company just agreed to merge with a larger firm, Lincoln Financial Corp (LNC), based in Philadelphia. He explained the upcoming annual meeting would be a chance to meet the new CEO in person. We should attend.

There are generally only two ways the life insurance business runs into trouble.

The first is estimating the mortality of people buying policies. The company uses actuaries, blood tests, physical exams, and every piece of data they can find on the person. Unexpected losses in this category are preventable.

The second way is tougher. It’s more unique to each life insurance company. It’s how management invests the float.

What we didn’t know in 2005 was these decisions on how to invest the float mattered more than ever. In less than three years we’d face a panic in the financial markets. The aggressive chase for yield meant most executives ignored risks in the runup years.

“Keep an Eye on Management”

Shareholders own the company. Even if you have a small number of shares, it’s your company.

All profits, dividends, and increases in the value of the company belong to the shareholders.

With ownership comes responsibility. Shareholders vote annually on company matters. They elect directors to represent them on the board, and approve major decisions.

My grandfather taught me the importance of shareholder voting, even with a tiny amount of stock. He told me, get the philosophy of ownership right, and everything else falls into place.

Most people buying stocks today don’t understand this. While they get a few trades right here and there, long-term success proves difficult.

Part of the problem is the buying process. It’s too easy. People hear about a stock. They plug the ticker symbol into an app on their phone. They buy one share and pay no commission. It’s about the same level of commitment as buying a raffle ticket for $2 hoping to win a convertible mustang spinning around at the casino entrance. To most people, it’s a sweepstakes. It’s entertainment.

But that’s not ownership. As a stock owner, you care about the overall health of your business. That means managing a delicate combination of stability and growth. Stable enough to survive a market swoon. Aggressive enough to grow faster than competitors.

Having the right leadership is the only way to do this. The overall economy, interest rates, or commodity prices affect every company. Management is the only truly unique feature of a company. It steers the ship.

In a perfect world, you’d meet the management team before buying any stock. It may not be practical. But it is possible.

As a stockholder, you have that right. And the annual meeting is a great place to do it.

A Weak Handshake

The outgoing JP CEO was a man named David Stonecipher. He looked like a combination of former fraternity president, and country club chairman. Appropriately dressed, confident, and welcoming, this guy made you feel like everything was fine. And in 2005, it was fine.

During his twelve-year tenure, he used the JP float to buy up other life insurance companies, office buildings, and a regional media company. Every televised college sporting event in North Carolina showed a Jefferson-Pilot company logo on the screen. As a JP stockholder, I felt like an owner just watching college basketball.

Stonecipher took the time to talk to me. I was a kid in my mid-20s, and he made me feel welcome. Then he said, “Come meet the new CEO.”

Here’s where things changed. I was too inexperienced to know exactly what I didn’t like about this guy, but something wasn’t right.

For starters, he seemed nervous. He reached out to shake my hand and I unintentionally overpowered him by about 50%. That’s never a good first impression. At least match the grip of the person you meet. It’s not a contest, but it should be obvious that we’re sizing each other up.

He didn’t recover from the handshake. I could tell right away this was a person most comfortable in a corporate structure. That’s fine for middle management, but the CEO faces external challenges, not just internal politics.

If I was right, we had a problem in the making. He might win internal turf wars, but this guy has a lot of float to invest. The value of my stock hung in the balance.

I felt like he would fire a younger version of outgoing CEO Stonecipher. He’d certainly fire me if I worked there. He’d replace us with loyal corporate serfs who didn’t threaten him.

When we left, my grandfather asked me, “What’d you think of that new CEO?” I said, “Not much.” He looked at me from the corner of his eyes and smirked…which is the polite way to make a point without saying too much.

90% Decline

The merger went through the following year. Two years after that I had a bad feeling about the stock. I called my grandfather to tell him I needed to sell.

To this day, I remember where I stood while making that call. He warned me about over-trading, being too jumpy. It leads at best to a big tax bill, and at worst losses.

I laid out my case, the stock was mine to sell. I respected him so much I compromised, agreeing to sell only a portion. I told him I’d buy it back in 60 days if I was wrong. That was the weekend of September 20, 2008.

Going against that wise counsel, I sold a portion of my LNC shares on Monday September 22 for an average price of ~$54. Seven weeks later, I bought them all back for ~$9.

Avoiding most of the collapse from high to low was one thing. Buying the stock back near the bottom proved lifechanging.

Everything went down during that period, even gold. But the market punished firms like LNC who ran with the herd, piling into fixed-rate debt and other financial products. That meant being caught in the middle of the 2008 market panic.

The following summer I sold the whole LNC position in the mid-$20s and used the proceeds to bet on myself. It kickstarted a wonderful career. I go into more detail on this in a new book, which should be out at the end of this quarter.

Our Virtual Disadvantage

The LNC trade changed my life. To be fair, it was 80% luck, and 20% the memory of that new CEO’s handshake. If I didn’t attend that final JP shareholder meeting, I might not have been so lucky.

You can’t shake hands on Zoom. That might be why companies want to get rid of in-person shareholder meetings all-together.

Having serving on several public boards in the past, I can tell you most CEOs would love to never deal with shareholder questions.

They quickly forget how things work. They think the company belongs to them; the shareholders are an inconvenience. The way I was taught:

Shareholders own the company

Shareholders elect directors

Directors hire management

Management runs the business

This is a perfect system of checks and balances. If the shareholder pays attention… And most don’t.

You might see mail pouring in this time of year from your broker. These large printed books, voting cards, and annual reports are important. Without them, that weak handshake drives the ship.

As a shareholder, the right to elect directors is critical. The larger a company grows, the more disconnected its directors become. It slowly shifts towards a diverse board of educators, retired politicians, and executives from other industries. This politically correct group often knows nothing about the industry. That means it can’t spot trouble in advance.

Management loves this type of board. The disconnected directors can’t supervise. During bad times, they blame the market. It’s job security, and if no one votes against it, it never changes.

I take the time to vote every proxy card that arrives at my office. I do the same for the trust.

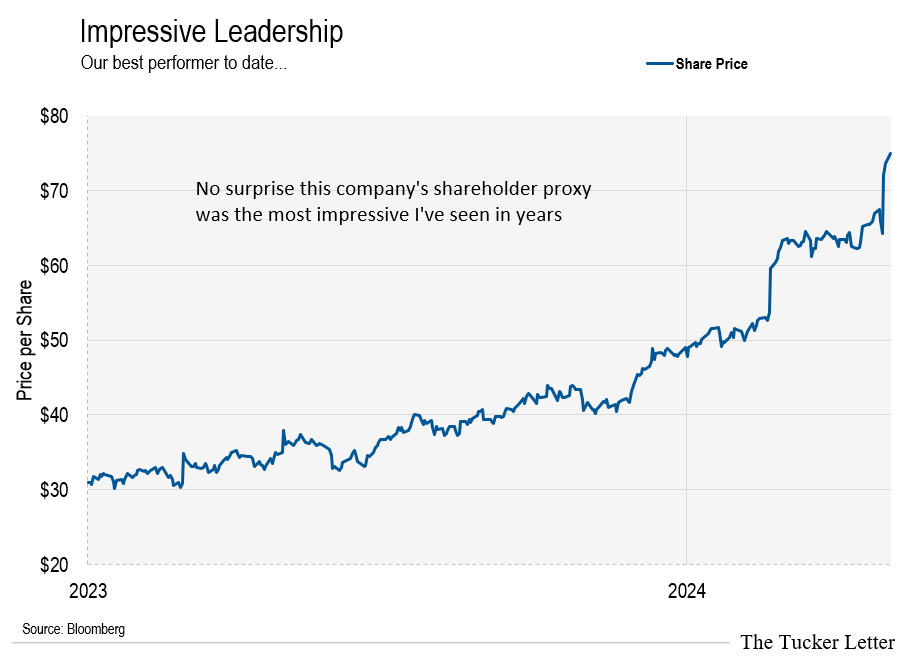

Our best performing stock in the Trustee Portfolio is up ~102% in 10 months. It’s a ~$7.4 billion market cap. When voting the proxy for the trust, I noticed something unique. Each director had a personalize bio next to their picture. They noted their favorite product produced by the company.

This was a personal touch, above and beyond normal requirements. It’s no surprise the company’s stock chart is straight up. Instead of wasting millions on excessive pay, corporate events, or a fancy headquarters, it invested in new facilities with enviable returns per square foot.

But that’s the exception. Most companies fall far short, with the share price following.

I attended the Campbell’s Soup Company (CPB) meeting in 2018 during a proxy fight. Dan Loeb tried to unseat the controlling shareholder, the Dorrance family. They keep a tight grip on the company. Loeb lost, and the stock went nowhere.

Plus, I saw the matriarch of the controlling shareholder family. She sat right in front of me. In addition to being uncomfortable around average people, she seemed agitated by Loeb’s attempt to disrupt her gravy train.

Campbell’s didn’t waste much money on the meeting. Any corporate event held next to a Super 8 Motel is one they hope you’ll skip.

And the recent trouble at Starbucks (SBUX) is no surprise to anyone who attended one of the company’s annual meetings like I did.

It felt like a rallying point for a socialist revolution. The ladies next to me went on and on about gender equality in stores. When they found out what I do, they asked if there would be more dividends next year.

Outside, protestors wore thousands of paper cups demanding an end to single-use containers.

Starbucks shares tumbled ~32% recently under dueling pressure of falling sales and rising costs. Just a few minutes at the shareholder meeting tells you stay away, unless we’re in a bull market.

But rising with a bull market is the easy way to run a company. It hardly justifies 7-figure incomes, excessive perks, and distance from shareholders. While we’ll leave bathroom equality to the protestors, we demand management who knows how to steer through turbulence. It’s possible, if we pay attention.

When you receive proxy cards in the mail this month, take the time to vote. At the very least, reward companies with a rising stock chart. Be more critical on the directors who supervised a tumbling share price.

Those voting cards are not junk mail, they’re the most powerful tool we have as investors.

Portfolio Review

Speaking of annual meetings, our most recent recommendation is up ~6.2% in the past two weeks.

The controlling family holds the reins using its class-B stock, which we discussed last issue. Each share has 10 votes compared to 1 for the class-A shares. While you can buy it, the A shares are more liquid, and better for the trust.

The company recently announced its annual shareholder meeting to be held on June 3, 2024 at 10:00 AM in Miami, FL. I plan to attend. I hope to meet the people steering the ship. They’ve delivered ~20% compounded annual returns for two decades. They deserve my voting support.